Progress with Patience

Week of May 9th, 2022

On-Chain Commentary

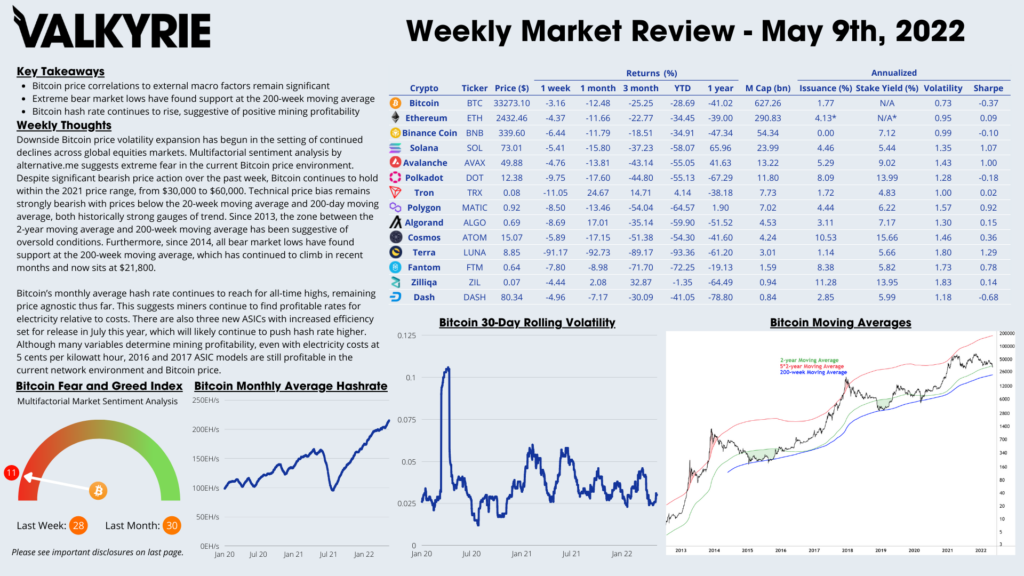

Downside Bitcoin price volatility expansion has begun in the setting of continued declines across global equities markets. Multifactorial sentiment analysis by alternative.me suggests extreme fear in the current Bitcoin price environment. Despite significant bearish price action over the past week, Bitcoin continues to hold within the 2021 price range, from $30,000 to $60,000. Technical price bias remains strongly bearish with prices below the 20-week moving average and 200-day moving average, both historically strong gauges of trend. Since 2013, the zone between the 2-year moving average and 200-week moving average has been suggestive of oversold conditions. Furthermore, since 2014, all bear market lows have found support at the 200-week moving average, which has continued to climb in recent months and now sits at $21,800.

Bitcoin’s monthly average hash rate continues to reach for all-time highs, remaining price agnostic thus far. This suggests miners continue to find profitable rates for electricity relative to costs. There are also three new ASICs with increased efficiency set for release in July this year, which will likely continue to push hash rate higher. Although many variables determine mining profitability, even with electricity costs at 5 cents per kilowatt hour, 2016 and 2017 ASIC models are still profitable in the current network environment and Bitcoin price

Macro Commentary

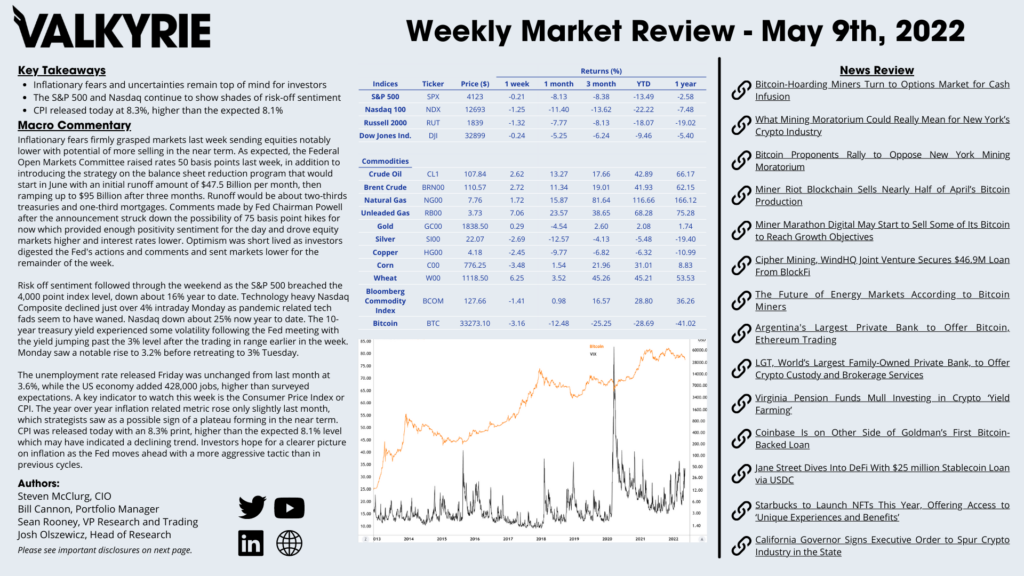

Inflationary fears firmly grasped markets last week sending equities notably lower with potential of more selling in the near term. As expected, the Federal Open Markets Committee raised rates 50 basis points last week, in addition to introducing the strategy on the balance sheet reduction program that would start in June with an initial runoff amount of $47.5 Billion per month, then ramping up to $95 Billion after three months. Runoff would be about two-thirds treasurys and one-third mortgages. Comments made by Fed Chairman Powell after the announcement struck down the possibility of 75 basis point hikes for now which provided enough positivity sentiment for the day and drove equity markets higher and interest rates lower. Optimism was short lived as investors digested the Fed’s actions and comments and sent markets lower for the remainder of the week.

Unemployment rate released Friday was unchanged from last month at 3.6%, while the US economy added 428 thousand jobs, higher than surveyed expectations. The year-over-year Consumer Price Index was released Wednesday morning at 8.3%, down from 8.5% last month. Core CPI also declined to 6.2% from 6.5% last month. Both numbers were slightly higher than surveyed expectations. Main headline was on the month-to-month Core CPI indication at 0.6%, up from 0.3% last month and higher than surveyed 0.4%. Markets initially reacted negatively but have returned to previous end of day levels, if not higher by late morning Wednesday. Focus turns to Thursday’s release of the Producer Price Index (PPI) which is experiencing a similar rise that correlates well to inflationary related measurement.

Risk off sentiment followed through the weekend as the S&P 500 breached the 4000 point index level, down about 16% year to date. Technology heavy Nasdaq Composite declined just over 4% intraday Monday as pandemic related tech fads seen to wane. Nasdaq down about 25% now year to date. The 10 year treasury yield experienced notable volatility following the Fed meeting with the yield jumping past the 3% level after the trading in range earlier in the week. Monday saw a rise to 3.2% before retreating to 3% Tuesday. Yield moved higher after CPI release but is unchanged mid-morning Wednesday.

Download the Full Weekly Market Review Here

The Portfolio Management Team

Steven McClurg, CIO

Bill Cannon, Portfolio Manager

Wes Cowan, Portfolio Manager, Head of Defi

Josh Olszewicz, Head of Research

Sean Rooney, VP Research and Trading

Will McDonough, Vice Chairman, Investment Committee

Leah Wald, CEO, Investment Committee

Shannon Smith, Head of Investor Relations