Macro Commentary

Key Takeaways

- Recession likelihood continues to increase based on key metrics

- CPI, PPI, and corporate earnings will help illuminate recession probability

- Unemployment numbers will be released Friday, exp. 3.6%, unchanged

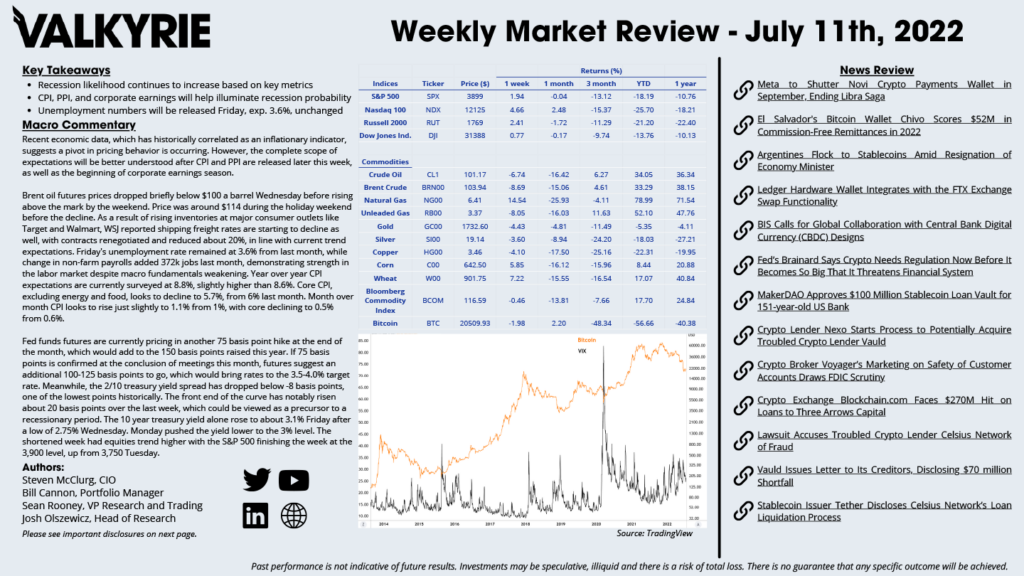

Recent economic data, which has historically correlated as an inflationary indicator, suggests a pivot in pricing behavior is occurring. However, the complete scope of expectations will be better understood after CPI and PPI are released later this week, as well as the beginning of corporate earnings season.

Brent oil futures prices dropped briefly below $100 a barrel Wednesday before rising above the mark by the weekend. Price was around $114 during the holiday weekend before the decline. As a result of rising inventories at major consumer outlets like Target and Walmart, WSJ reported shipping freight rates are starting to decline as well, with contracts renegotiated and reduced about 20%, in line with current trend expectations. Friday’s unemployment rate remained at 3.6% from last month, while change in non-farm payrolls added 372k jobs last month, demonstrating strength in the labor market despite macro fundamentals weakening. Year over year CPI expectations are currently surveyed at 8.8%, slightly higher than 8.6%. Core CPI, excluding energy and food, looks to decline to 5.7%, from 6% last month. Month over month CPI looks to rise just slightly to 1.1% from 1%, with core declining to 0.5% from 0.6%.

Fed funds futures are currently pricing in another 75 basis point hike at the end of the month, which would add to the 150 basis points raised this year. If 75 basis points is confirmed at the conclusion of meetings this month, futures suggest an additional 100-125 basis points to go, which would bring rates to the 3.5-4.0% target rate. Meanwhile, the 2/10 treasury yield spread has dropped below -8 basis points, one of the lowest points historically. The front end of the curve has notably risen about 20 basis points over the last week, which could be viewed as a precursor to a recessionary period. The 10 year treasury yield alone rose to about 3.1% Friday after a low of 2.75% Wednesday. Monday pushed the yield lower to the 3% level. The shortened week had equities trend higher with the S&P 500 finishing the week at the 3,900 level, up from 3,750 Tuesday.

this Friday, currently surveyed to remain unchanged at 3.6%. Next FOMC meeting is at the end of the month.

On-Chain Commentary

Key Takeaways

- Leverage continues to unwind with crypto lenders liquidating collateral to cash

- Technicals dating back to Bitcoin’s inception show price maintaining key levels

- Industrial Bitcoin miners in Texas are curtailing use over grid concerns

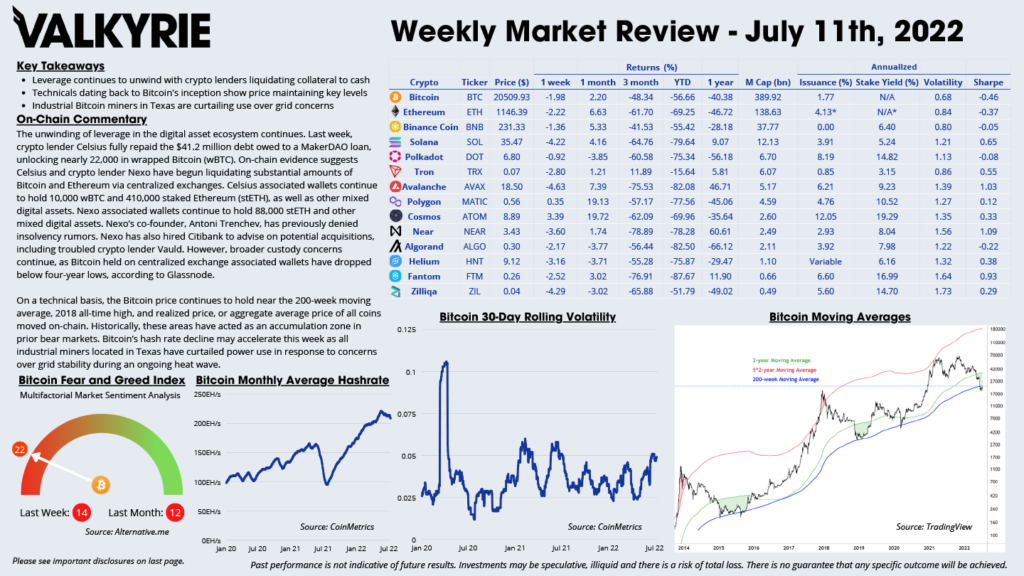

The unwinding of leverage in the digital asset ecosystem continues. Last week, crypto lender Celsius fully repaid the $41.2 million debt owed to a MakerDAO loan, unlocking nearly 22,000 in wrapped Bitcoin (wBTC). On-chain evidence suggests Celsius and crypto lender Nexo have begun liquidating substantial amounts of Bitcoin and Ethereum via centralized exchanges. Celsius associated wallets continue to hold 10,000 wBTC and 410,000 staked Ethereum (stETH), as well as other mixed digital assets. Nexo associated wallets continue to hold 88,000 stETH and other mixed digital assets. Nexo’s co-founder, Antoni Trenchev, has previously denied insolvency rumors. Nexo has also hired Citibank to advise on potential acquisitions, including troubled crypto lender Vauld. However, broader custody concerns continue, as Bitcoin held on centralized exchange associated wallets have dropped below four-year lows, according to Glassnode.

On a technical basis, the Bitcoin price continues to hold near the 200-week moving average, 2018 all-time high, and realized price, or aggregate average price of all coins moved on-chain. Historically, these areas have acted as an accumulation zone in prior bear markets. Bitcoin’s hash rate decline may accelerate this week as all industrial miners located in Texas have curtailed power use in response to concerns over grid stability during an ongoing heat wave.

Download the Full Weekly Market Review Here

The Portfolio Management Team

Steven McClurg, CIO

Bill Cannon, Portfolio Manager

Wes Cowan, Portfolio Manager, Head of Defi

Josh Olszewicz, Head of Research

Sean Rooney, VP Research and Trading

Will McDonough, Vice Chairman, Investment Committee

Leah Wald, CEO, Investment Committee

Shannon Smith, Head of Investor Relations