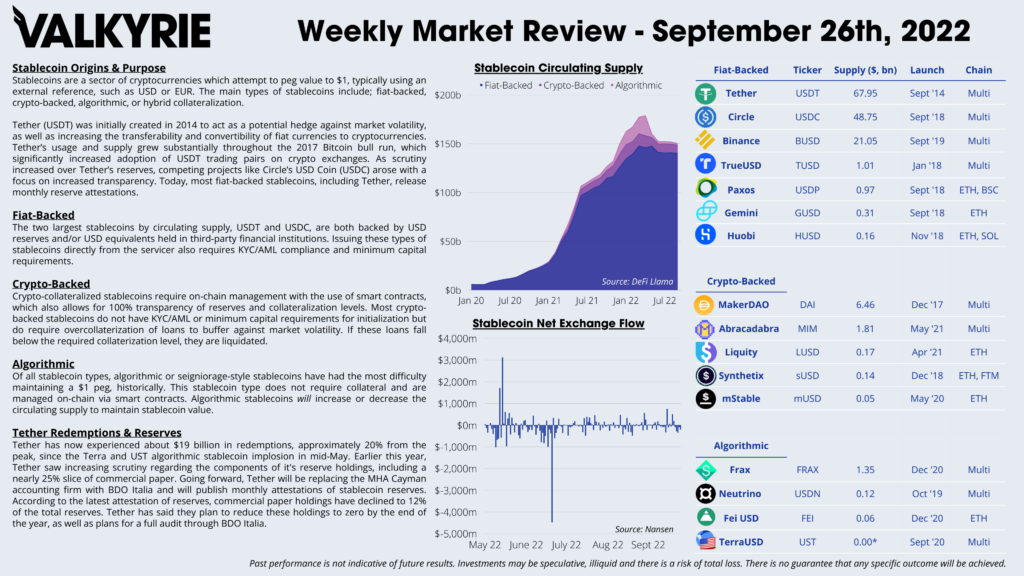

Traditional Market Commentary

- In regards to hikes, markets continue to be more optimistic than reality

- Probabilities for the year-end terminal rate stands at 4.50-4.75%

- Strains in the Forex markets rise as the dollar continues to strengthen

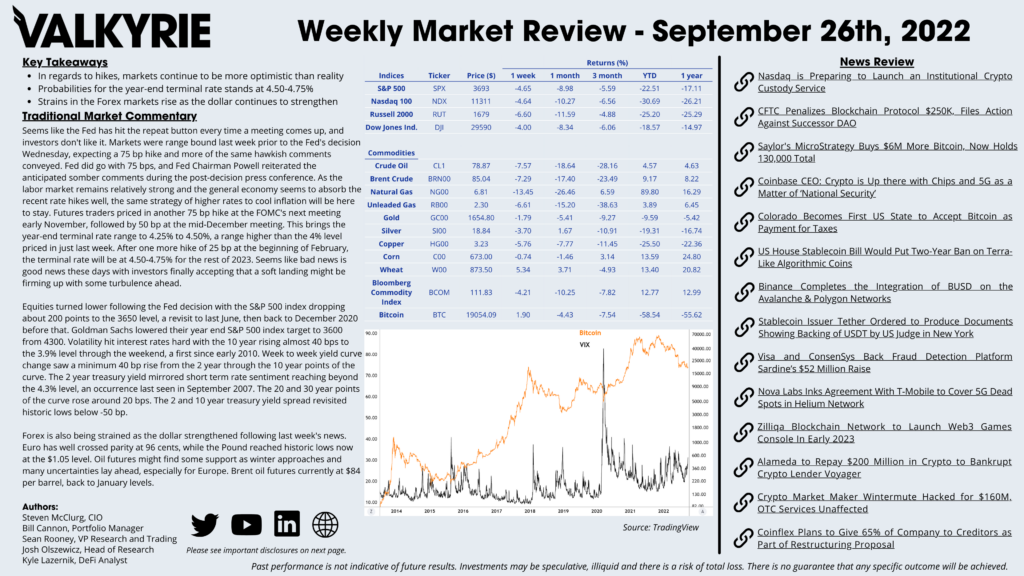

Seems like the Fed has hit the repeat button every time a meeting comes up, and investors don’t like it. Markets were range bound last week prior to the Fed’s decision Wednesday, expecting a 75 bp hike and more of the same hawkish comments conveyed. Fed did go with 75 bps, and Fed Chairman Powell reiterated the anticipated somber comments during the post-decision press conference. As the labor market remains relatively strong and the general economy seems to absorb the recent rate hikes well, the same strategy of higher rates to cool inflation will be here to stay. Futures traders priced in another 75 bp hike at the FOMC’s next meeting early November, followed by 50 bp at the mid-December meeting. This brings the year-end terminal rate range to 4.25% to 4.50%, a range higher than the 4% level priced in just last week. After one more hike of 25 bp at the beginning of February, the terminal rate will be at 4.50-4.75% for the rest of 2023. Seems like bad news is good news these days with investors finally accepting that a soft landing might be firming up with some turbulence ahead.

Equities turned lower following the Fed decision with the S&P 500 index dropping about 200 points to the 3650 level, a revisit to last June, then back to December 2020 before that. Goldman Sachs lowered their year end S&P 500 index target to 3600 from 4300. Volatility hit interest rates hard with the 10 year rising almost 40 bps to the 3.9% level through the weekend, a first since early 2010. Week to week yield curve change saw a minimum 40 bp rise from the 2 year through the 10 year points of the curve. The 2 year treasury yield mirrored short term rate sentiment reaching beyond the 4.3% level, an occurrence last seen in September 2007. The 20 and 30 year points of the curve rose around 20 bps. The 2 and 10 year treasury yield spread revisited historic lows below -50 bp.

Forex is also being strained as the dollar strengthened following last week’s news. Euro has well crossed parity at 96 cents, while the Pound reached historic lows now at the $1.05 level. Oil futures might find some support as winter approaches and many uncertainties lay ahead, especially for Europe. Brent oil futures currently at $84 per barrel, back to January levels.

On-Chain Commentary

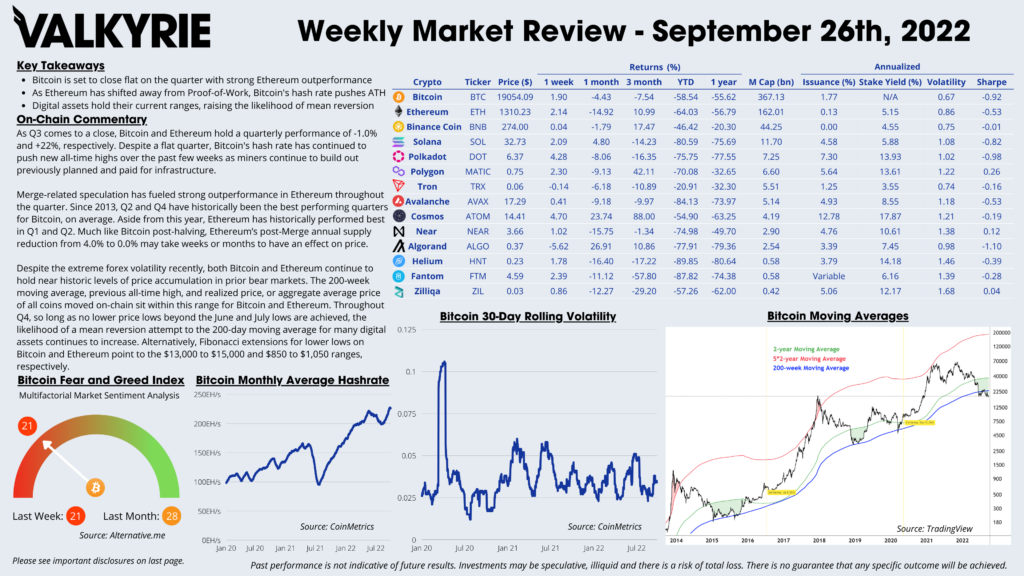

- Bitcoin is set to close flat on the quarter with strong Ethereum outperformance

- As Ethereum has shifted away from Proof-of-Work, Bitcoin’s hash rate pushes ATH

- Digital assets hold their current ranges, raising the likelihood of mean reversion

As Q3 comes to a close, Bitcoin and Ethereum hold a quarterly performance of -1.0% and +22%, respectively. Despite a flat quarter, Bitcoin’s hash rate has continued to push new all-time highs over the past few weeks as miners continue to build out previously planned and paid for infrastructure.

Merge-related speculation has fueled strong outperformance in Ethereum throughout the quarter. Since 2013, Q2 and Q4 have historically been the best performing quarters for Bitcoin, on average. Aside from this year, Ethereum has historically performed best in Q1 and Q2. Much like Bitcoin post-halving, Ethereum’s post-Merge annual supply reduction from 4.0% to 0.0% may take weeks or months to have an effect on price.

Despite the extreme forex volatility recently, both Bitcoin and Ethereum continue to hold near historic levels of price accumulation in prior bear markets. The 200-week moving average, previous all-time high, and realized price, or aggregate average price of all coins moved on-chain sit within this range for Bitcoin and Ethereum. Throughout Q4, so long as no lower price lows beyond the June and July lows are achieved, the likelihood of a mean reversion attempt to the 200-day moving average for many digital assets continues to increase. Alternatively, Fibonacci extensions for lower lows on Bitcoin and Ethereum point to the $13,000 to $15,000 and $850 to $1,050 ranges, respectively.

DeFi Commentary

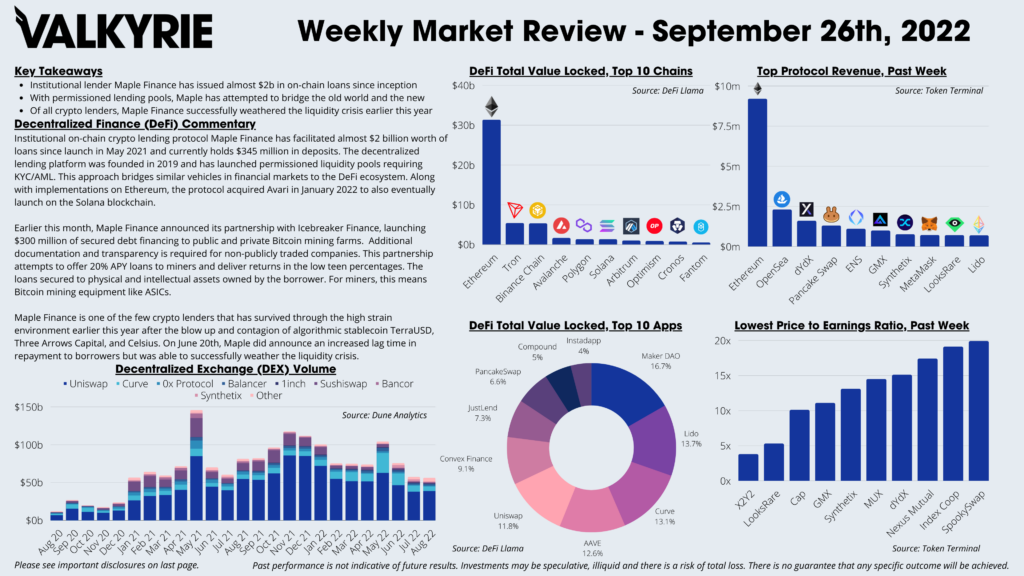

- Institutional lender Maple Finance has issued almost $2b in on-chain loans since inception

- With permissioned lending pools, Maple has attempted to bridge the old world and the new

- Of all crypto lenders, Maple Finance successfully weathered the liquidity crisis earlier this year

Institutional on-chain crypto lending protocol Maple Finance has facilitated almost $2 billion worth of loans since launch in May 2021 and currently holds $345 million in deposits. The decentralized lending platform was founded in 2019 and has launched permissioned liquidity pools requiring KYC/AML. This approach bridges similar vehicles in financial markets to the DeFi ecosystem. Along with implementations on Ethereum, the protocol acquired Avari in January 2022 to also eventually launch on the Solana blockchain.

Earlier this month, Maple Finance announced its partnership with Icebreaker Finance, launching $300 million of secured debt financing to public and private Bitcoin mining farms. Additional documentation and transparency is required for non-publicly traded companies. This partnership attempts to offer 20% APY loans to miners and deliver returns in the low teen percentages. The loans secured to physical and intellectual assets owned by the borrower. For miners, this means Bitcoin mining equipment like ASICs.

Maple Finance is one of the few crypto lenders that has survived through the high strain environment earlier this year after the blow up and contagion of algorithmic stablecoin TerraUSD, Three Arrows Capital, and Celsius. On June 20th, Maple did announce an increased lag time in repayment to borrowers but was able to successfully weather the liquidity crisis.

Download the Full Weekly Market Review Here