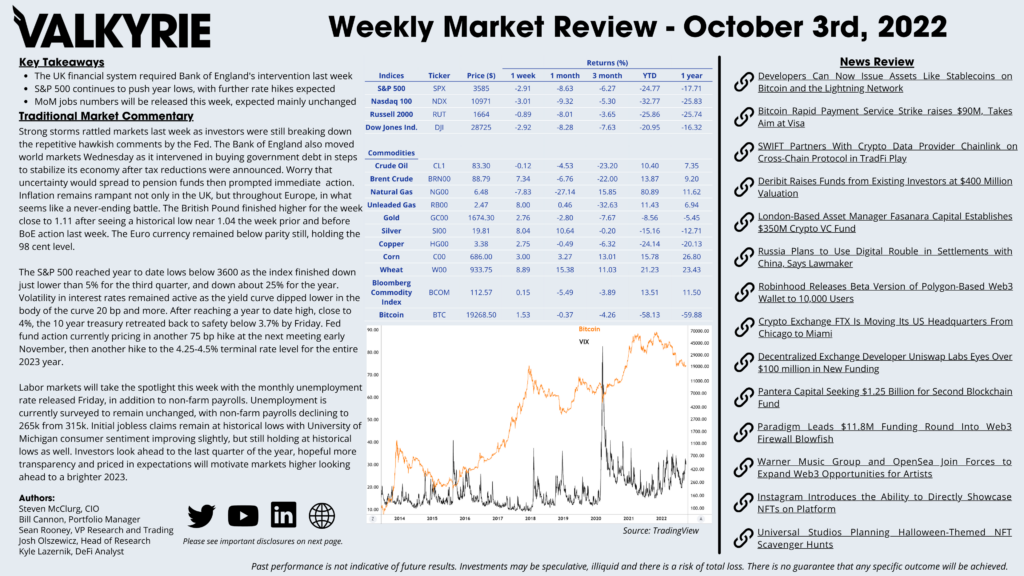

Traditional Market Commentary

- The UK financial system required Bank of England’s intervention last week

- S&P 500 continues to push year lows, with further rate hikes expected

- MoM jobs numbers will be released this week, expected mainly unchanged

Strong storms rattled markets last week as investors were still breaking down the repetitive hawkish comments by the Fed. The Bank of England also moved world markets Wednesday as it intervened in buying government debt in steps to stabilize its economy after tax reductions were announced. Worry that uncertainty would spread to pension funds then prompted immediate action. Inflation remains rampant not only in the UK, but throughout Europe, in what seems like a never-ending battle. The British Pound finished higher for the week close to 1.11 after seeing a historical low near 1.04 the week prior and before BoE action last week. The Euro currency remained below parity still, holding the 98 cent level.

The S&P 500 reached year to date lows below 3600 as the index finished down just lower than 5% for the third quarter, and down about 25% for the year. Volatility in interest rates remained active as the yield curve dipped lower in the body of the curve 20 bp and more. After reaching a year to date high, close to 4%, the 10 year treasury retreated back to safety below 3.7% by Friday. Fed fund action currently pricing in another 75 bp hike at the next meeting early November, then another hike to the 4.25-4.5% terminal rate level for the entire 2023 year.

Labor markets will take the spotlight this week with the monthly unemployment rate released Friday, in addition to non-farm payrolls. Unemployment is currently surveyed to remain unchanged, with non-farm payrolls declining to 265k from 315k. Initial jobless claims remain at historical lows with University of Michigan consumer sentiment improving slightly, but still holding at historical lows as well. Investors look ahead to the last quarter of the year, hopeful more transparency and priced in expectations will motivate markets higher looking ahead to a brighter 2023.

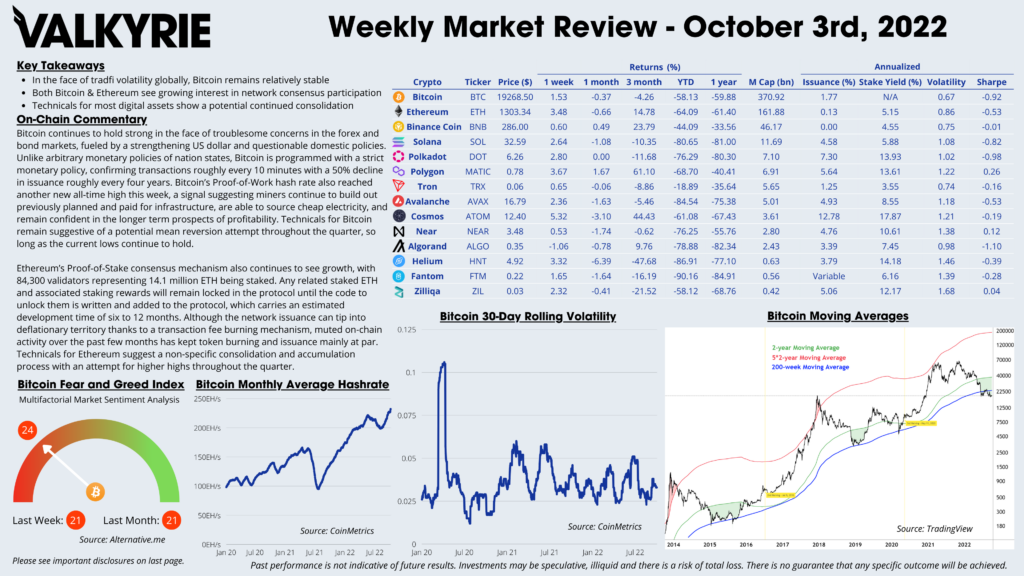

On-Chain Commentary

- In the face of tradfi volatility globally, Bitcoin remains relatively stable

- Both Bitcoin & Ethereum see growing interest in network consensus participation

- Technicals for most digital assets show a potential continued consolidation

Bitcoin continues to hold strong in the face of troublesome concerns in the forex and bond markets, fueled by a strengthening US dollar and questionable domestic policies. Unlike arbitrary monetary policies of nation states, Bitcoin is programmed with a strict monetary policy, confirming transactions roughly every 10 minutes with a 50% decline in issuance roughly every four years. Bitcoin’s Proof-of-Work hash rate also reached another new all-time high this week, a signal suggesting miners continue to build out previously planned and paid for infrastructure, are able to source cheap electricity, and remain confident in the longer term prospects of profitability. Technicals for Bitcoin remain suggestive of a potential mean reversion attempt throughout the quarter, so long as the current lows continue to hold.

Ethereum’s Proof-of-Stake consensus mechanism also continues to see growth, with 84,300 validators representing 14.1 million ETH being staked. Any related staked ETH and associated staking rewards will remain locked in the protocol until the code to unlock them is written and added to the protocol, which carries an estimated development time of six to 12 months. Although the network issuance can tip into deflationary territory thanks to a transaction fee burning mechanism, muted on-chain activity over the past few months has kept token burning and issuance mainly at par. Technicals for Ethereum suggest a non-specific consolidation and accumulation process with an attempt for higher highs throughout the quarter.

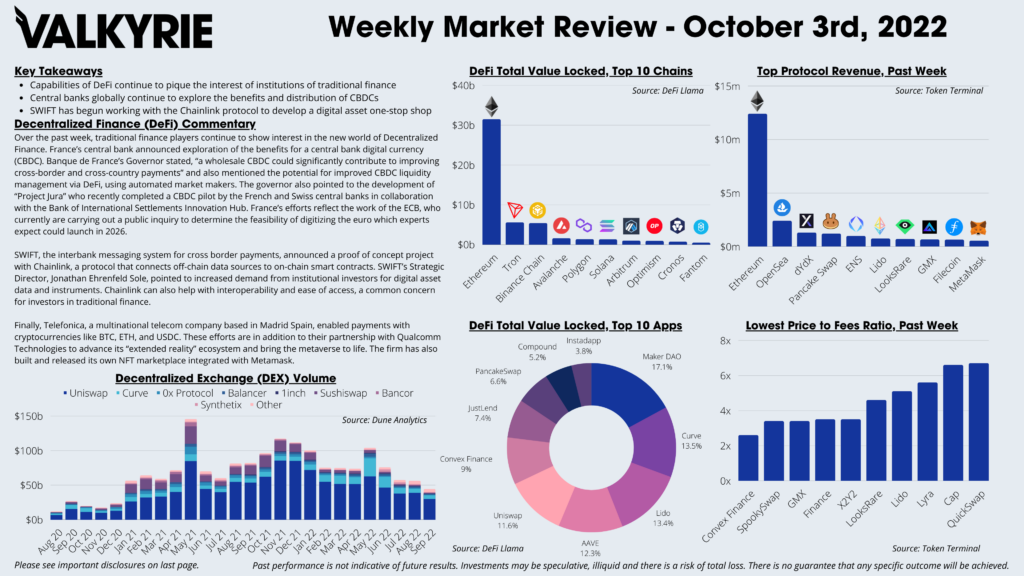

DeFi Commentary

- Capabilities of DeFi continue to pique the interest of institutions of traditional finance

- Central banks globally continue to explore the benefits and distribution of CBDCs

- SWIFT has begun working with the Chainlink protocol to develop a digital asset one-stop shop

Over the past week, traditional finance players continue to show interest in the new world of Decentralized Finance. France’s central bank announced exploration of the benefits for a central bank digital currency (CBDC). Banque de France’s Governor stated, “a wholesale CBDC could significantly contribute to improving cross-border and cross-country payments” and also mentioned the potential for improved CBDC liquidity management via DeFi, using automated market makers. The governor also pointed to the development of “Project Jura” who recently completed a CBDC pilot by the French and Swiss central banks in collaboration with the Bank of International Settlements Innovation Hub. France’s efforts reflect the work of the ECB, who currently are carrying out a public inquiry to determine the feasibility of digitizing the euro which experts expect could launch in 2026.

SWIFT, the interbank messaging system for cross border payments, announced a proof of concept project with Chainlink, a protocol that connects off-chain data sources to on-chain smart contracts. SWIFT’s Strategic Director, Jonathan Ehrenfeld Sole, pointed to increased demand from institutional investors for digital asset data and instruments. Chainlink can also help with interoperability and ease of access, a common concern for investors in traditional finance.

Finally, Telefonica, a multinational telecom company based in Madrid Spain, enabled payments with cryptocurrencies like BTC, ETH, and USDC. These efforts are in addition to their partnership with Qualcomm Technologies to advance its “extended reality” ecosystem and bring the metaverse to life. The firm has also built and released its own NFT marketplace integrated with Metamask.

Download the Full Weekly Market Review Here