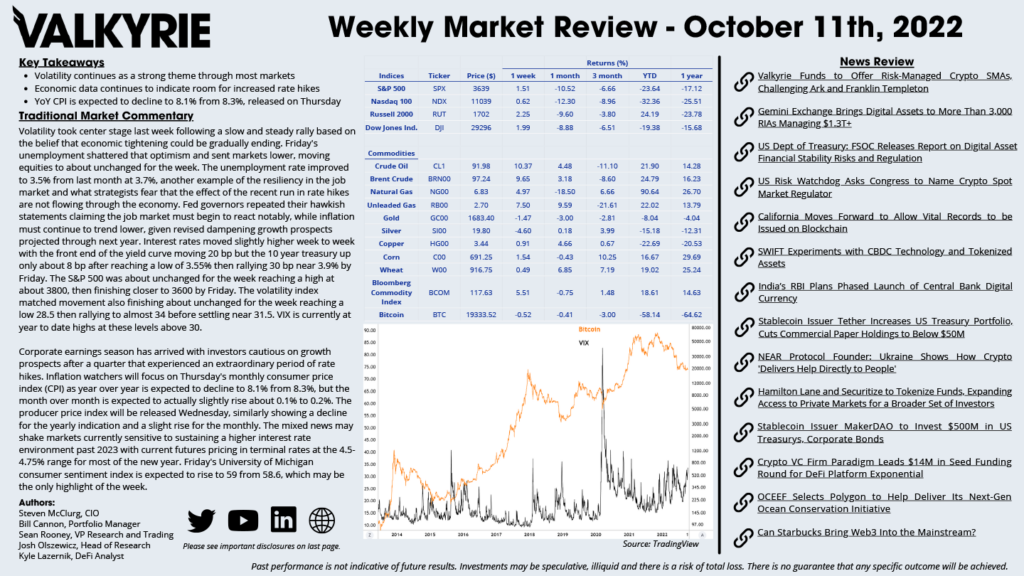

Traditional Market Commentary

- Volatility continues as a strong theme through most markets

- Economic data continues to indicate room for increased rate hikes

- YoY CPI is expected to decline to 8.1% from 8.3%, released on Thursday

Volatility took center stage last week following a slow and steady rally based on the belief that economic tightening could be gradually ending. Friday’s unemployment shattered that optimism and sent markets lower, moving equities to about unchanged for the week. The unemployment rate improved to 3.5% from last month at 3.7%, another example of the resiliency in the job market and what strategists fear that the effect of the recent run in rate hikes are not flowing through the economy. Fed governors repeated their hawkish statements claiming the job market must begin to react notably, while inflation must continue to trend lower, given revised dampening growth prospects projected through next year. Interest rates moved slightly higher week to week with the front end of the yield curve moving 20 bp but the 10 year treasury up only about 8 bp after reaching a low of 3.55% then rallying 30 bp near 3.9% by Friday. The S&P 500 was about unchanged for the week reaching a high at about 3800, then finishing closer to 3600 by Friday. The volatility index matched movement also finishing about unchanged for the week reaching a low 28.5 then rallying to almost 34 before settling near 31.5. VIX is currently at year to date highs at these levels above 30.

Corporate earnings season has arrived with investors cautious on growth prospects after a quarter that experienced an extraordinary period of rate hikes. Inflation watchers will focus on Thursday’s monthly consumer price index (CPI) as year over year is expected to decline to 8.1% from 8.3%, but the month over month is expected to actually slightly rise about 0.1% to 0.2%. The producer price index will be released Wednesday, similarly showing a decline for the yearly indication and a slight rise for the monthly. The mixed news may shake markets currently sensitive to sustaining a higher interest rate environment past 2023 with current futures pricing in terminal rates at the 4.5-4.75% range for most of the new year. Friday’s University of Michigan consumer sentiment index is expected to rise to 59 from 58.6, which may be the only highlight of the week.

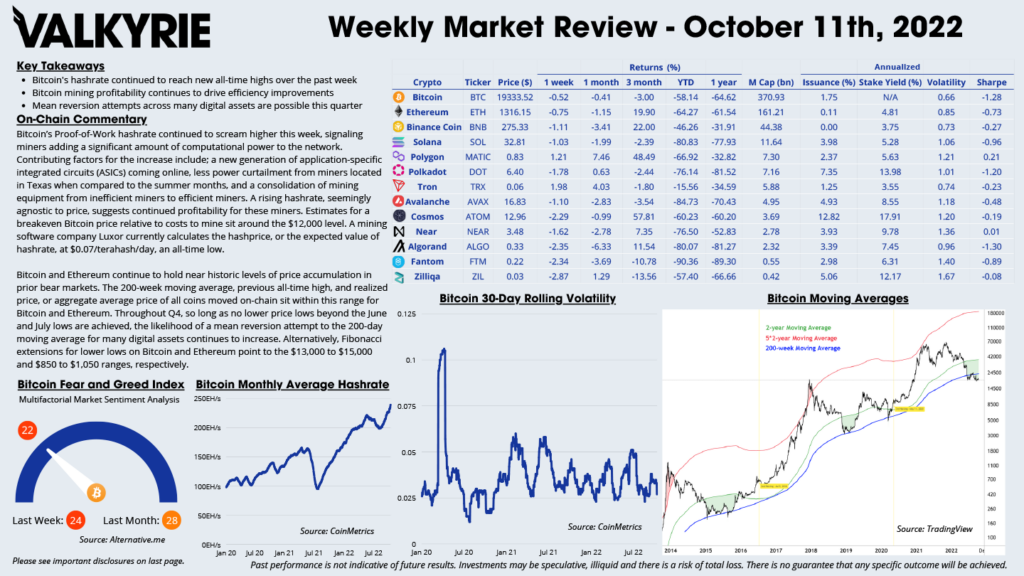

On-Chain Commentary

- Bitcoin’s hashrate continued to reach new all-time highs over the past week

- Bitcoin mining profitability continues to drive efficiency improvements

- Mean reversion attempts across many digital assets are possible this quarter

Bitcoin’s Proof-of-Work hashrate continued to scream higher this week, signaling miners adding a significant amount of computational power to the network. Contributing factors for the increase include; a new generation of application-specific integrated circuits (ASICs) coming online, less power curtailment from miners located in Texas when compared to the summer months, and a consolidation of mining equipment from inefficient miners to efficient miners. A rising hashrate, seemingly agnostic to price, suggests continued profitability for these miners. Estimates for a breakeven Bitcoin price relative to costs to mine sit around the $12,000 level. A mining software company Luxor currently calculates the hashprice, or the expected value of hashrate, at $0.07/terahash/day, an all-time low.

Bitcoin and Ethereum continue to hold near historic levels of price accumulation in prior bear markets. The 200-week moving average, previous all-time high, and realized price, or aggregate average price of all coins moved on-chain sit within this range for Bitcoin and Ethereum. Throughout Q4, so long as no lower price lows beyond the June and July lows are achieved, the likelihood of a mean reversion attempt to the 200-day moving average for many digital assets continues to increase. Alternatively, Fibonacci extensions for lower lows on Bitcoin and Ethereum point to the $13,000 to $15,000 and $850 to $1,050 ranges, respectively.

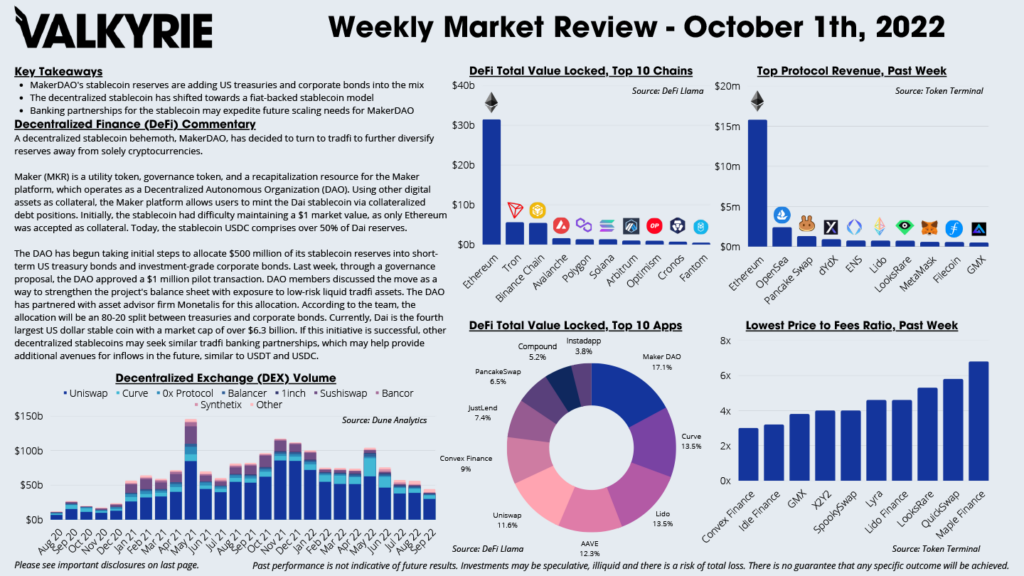

DeFi Commentary

- MakerDAO’s stablecoin reserves are adding US treasuries and corporate bonds into the mix

- The decentralized stablecoin has shifted towards a fiat-backed stablecoin model

- Banking partnerships for the stablecoin may expedite future scaling needs for MakerDAO

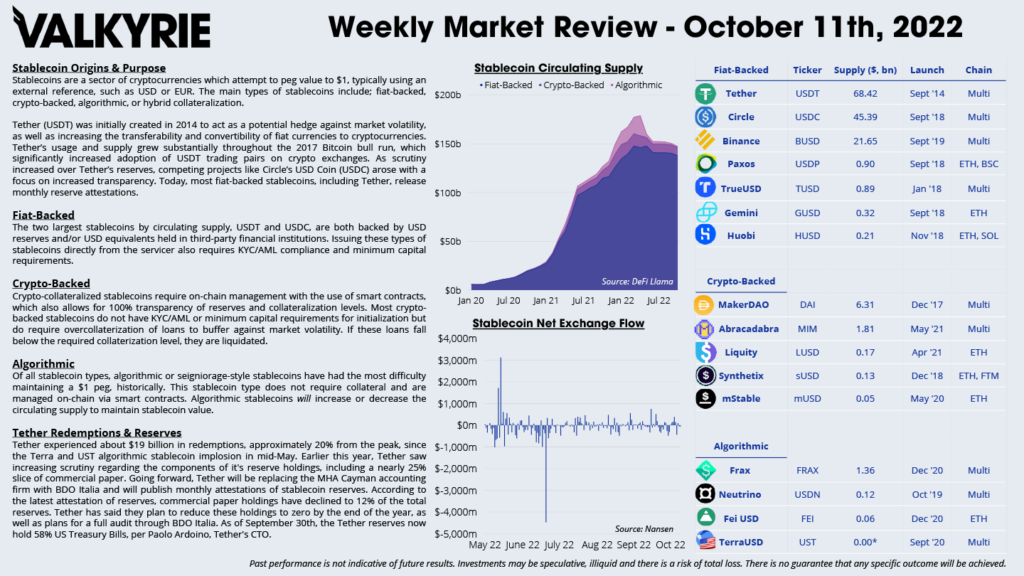

A decentralized stablecoin behemoth, MakerDAO, has decided to turn to tradfi to further diversify reserves away from solely cryptocurrencies.

Maker (MKR) is a utility token, governance token, and a recapitalization resource for the Maker platform, which operates as a Decentralized Autonomous Organization (DAO). Using other digital assets as collateral, the Maker platform allows users to mint the Dai stablecoin via collateralized debt positions. Initially, the stablecoin had difficulty maintaining a $1 market value, as only Ethereum was accepted as collateral. Today, the stablecoin USDC comprises over 50% of Dai reserves.

The DAO has begun taking initial steps to allocate $500 million of its stablecoin reserves into short-term US treasury bonds and investment-grade corporate bonds. Last week, through a governance proposal, the DAO approved a $1 million pilot transaction. DAO members discussed the move as a way to strengthen the project’s balance sheet with exposure to low-risk liquid tradfi assets. The DAO has partnered with asset advisor firm Monetalis for this allocation. According to the team, the allocation will be an 80-20 split between treasuries and corporate bonds. Currently, Dai is the fourth largest US dollar stable coin with a market cap of over $6.3 billion. If this initiative is successful, other decentralized stablecoins may seek similar tradfi banking partnerships, which may help provide additional avenues for inflows in the future, similar to USDT and USDC.

Download the Full Weekly Market Review Here