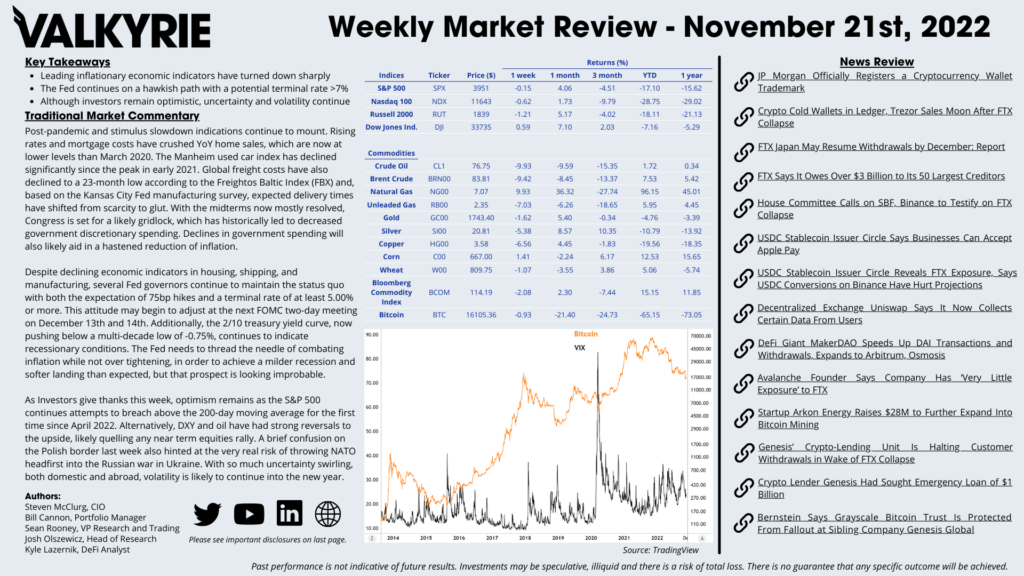

Traditional Market Commentary

- Leading inflationary economic indicators have turned down sharply

- The Fed continues on a hawkish path with a potential terminal rate >7%

- Although investors remain optimistic, uncertainty and volatility continue

Post-pandemic and stimulus slowdown indications continue to mount. Rising rates and mortgage costs have crushed YoY home sales, which are now at lower levels than March 2020. The Manheim used car index has declined significantly since the peak in early 2021. Global freight costs have also declined to a 23-month low according to the Freightos Baltic Index (FBX) and, based on the Kansas City Fed manufacturing survey, expected delivery times have shifted from scarcity to glut. With the midterms now mostly resolved, Congress is set for a likely gridlock, which has historically led to decreased government discretionary spending. Declines in government spending will also likely aid in a hastened reduction of inflation.

Despite declining economic indicators in housing, shipping, and manufacturing, several Fed governors continue to maintain the status quo with both the expectation of 75bp hikes and a terminal rate of at least 5.00% or more. This attitude may begin to adjust at the next FOMC two-day meeting on December 13th and 14th. Additionally, the 2/10 treasury yield curve, now pushing below a multi-decade low of -0.75%, continues to indicate recessionary conditions. The Fed needs to thread the needle of combating inflation while not over tightening, in order to achieve a milder recession and softer landing than expected, but that prospect is looking improbable.

As Investors give thanks this week, optimism remains as the S&P 500 continues attempts to breach above the 200-day moving average for the first time since April 2022. Alternatively, DXY and oil have had strong reversals to the upside, likely quelling any near term equities rally. A brief confusion on the Polish border last week also hinted at the very real risk of throwing NATO headfirst into the Russian war in Ukraine. With so much uncertainty swirling, both domestic and abroad, volatility is likely to continue into the new year.

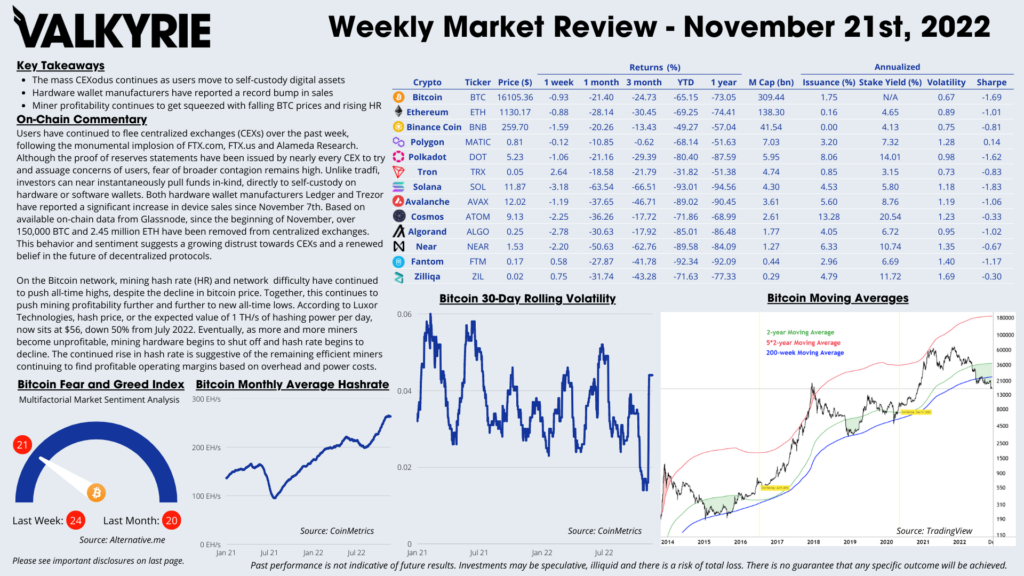

On-Chain Commentary

- The mass CEXodus continues as users move to self-custody digital assets

- Hardware wallet manufacturers have reported a record bump in sales

- Miner profitability continues to get squeezed with falling BTC prices and rising HR

Users have continued to flee centralized exchanges (CEXs) over the past week, following the monumental implosion of FTX.com, FTX.us and Alameda Research. Although the proof of reserves statements have been issued by nearly every CEX to try and assuage concerns of users, fear of broader contagion remains high. Unlike tradfi, investors can near instantaneously pull funds in-kind, directly to self-custody on hardware or software wallets. Both hardware wallet manufacturers Ledger and Trezor have reported a significant increase in device sales since November 7th. Based on available on-chain data from Glassnode, since the beginning of November, over 150,000 BTC and 2.45 million ETH have been removed from centralized exchanges. This behavior and sentiment suggests a growing distrust towards CEXs and a renewed belief in the future of decentralized protocols.

On the Bitcoin network, mining hash rate (HR) and network difficulty have continued to push all-time highs, despite the decline in bitcoin price. Together, this continues to push mining profitability further and further to new all-time lows. According to Luxor Technologies, hash price, or the expected value of 1 TH/s of hashing power per day, now sits at $56, down 50% from July 2022. Eventually, as more and more miners become unprofitable, mining hardware begins to shut off and hash rate begins to decline. The continued rise in hash rate is suggestive of the remaining efficient miners continuing to find profitable operating margins based on overhead and power costs.