On-Chain Commentary

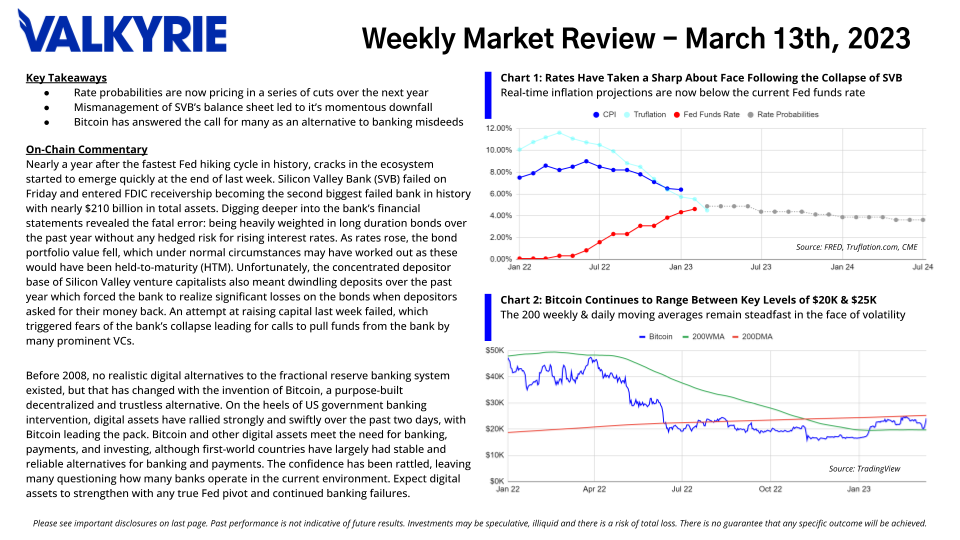

- Rate probabilities are now pricing in a series of cuts over the next year

- Mismanagement of SVB’s balance sheet led to it’s momentous downfall

- Bitcoin has answered the call for many as an alternative to banking misdeeds

Nearly a year after the fastest Fed hiking cycle in history, cracks in the ecosystem started to emerge quickly at the end of last week. Silicon Valley Bank (SVB) failed on Friday and entered FDIC receivership becoming the second biggest failed bank in history with nearly $210 billion in total assets. Digging deeper into the bank’s financial statements revealed the fatal error: being heavily weighted in long duration bonds over the past year without any hedged risk for rising interest rates. As rates rose, the bond portfolio value fell, which under normal circumstances may have worked out as these would have been held-to-maturity (HTM). Unfortunately, the concentrated depositor base of Silicon Valley venture capitalists also meant dwindling deposits over the past year which forced the bank to realize significant losses on the bonds when depositors asked for their money back. An attempt at raising capital last week failed, which triggered fears of the bank’s collapse leading for calls to pull funds from the bank by many prominent VCs.

Before 2008, no realistic digital alternatives to the fractional reserve banking system existed, but that has changed with the invention of Bitcoin, a purpose-built decentralized and trustless alternative. On the heels of US government banking intervention, digital assets have rallied strongly and swiftly over the past two days, with Bitcoin leading the pack. Bitcoin and other digital assets meet the need for banking, payments, and investing, although first-world countries have largely had stable and reliable alternatives for banking and payments. The confidence has been rattled, leaving many questioning how many banks operate in the current environment. Expect digital assets to strengthen with any true Fed pivot and continued banking failures.