Macro Commentary

Key Takeaways

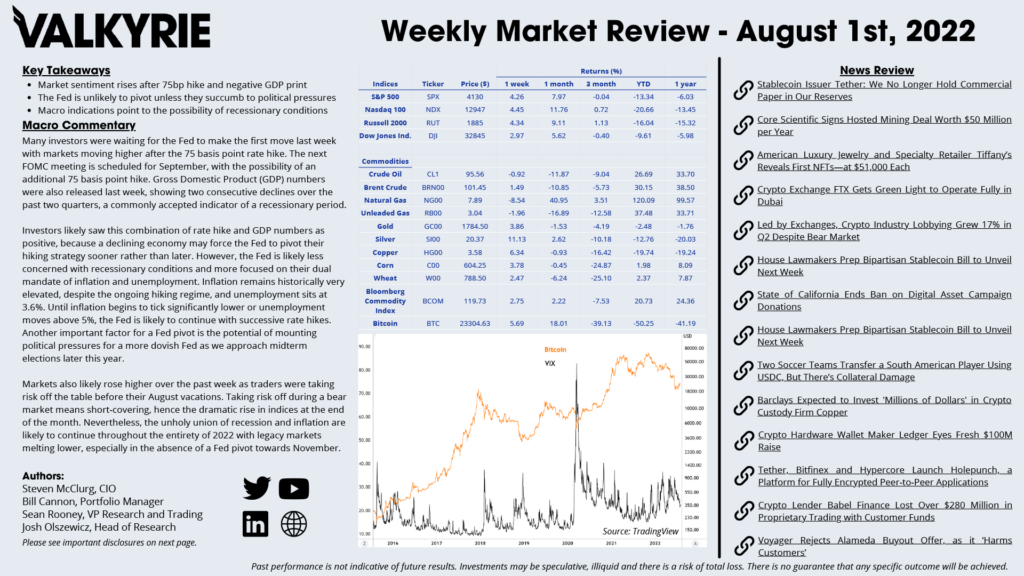

- Market sentiment rises after 75bp hike and negative GDP print

- The Fed is unlikely to pivot unless they succumb to political pressures

- Macro indications point to the possibility of recessionary conditions

Many investors were waiting for the Fed to make the first move last week with markets moving higher after the 75 basis point rate hike. The next FOMC meeting is scheduled for September, with the possibility of an additional 75 basis point hike. Gross Domestic Product (GDP) numbers were also released last week, showing two consecutive declines over the past two quarters, a commonly accepted indicator of a recessionary period.

Investors likely saw this combination of rate hike and GDP numbers as positive, because a declining economy may force the Fed to pivot their hiking strategy sooner rather than later. However, the Fed is likely less concerned with recessionary conditions and more focused on their dual mandate of inflation and unemployment. Inflation remains historically very elevated, despite the ongoing hiking regime, and unemployment sits at 3.6%. Until inflation begins to tick significantly lower or unemployment moves above 5%, the Fed is likely to continue with successive rate hikes. Another important factor for a Fed pivot is the potential of mounting political pressures for a more dovish Fed as we approach midterm elections later this year.

Markets also likely rose higher over the past week as traders were taking risk off the table before their August vacations. Taking risk off during a bear market means short-covering, hence the dramatic rise in indices at the end of the month. Nevertheless, the unholy union of recession and inflation are likely to continue throughout the entirety of 2022 with legacy markets melting lower, especially in the absence of a Fed pivot towards November.

On-Chain Commentary

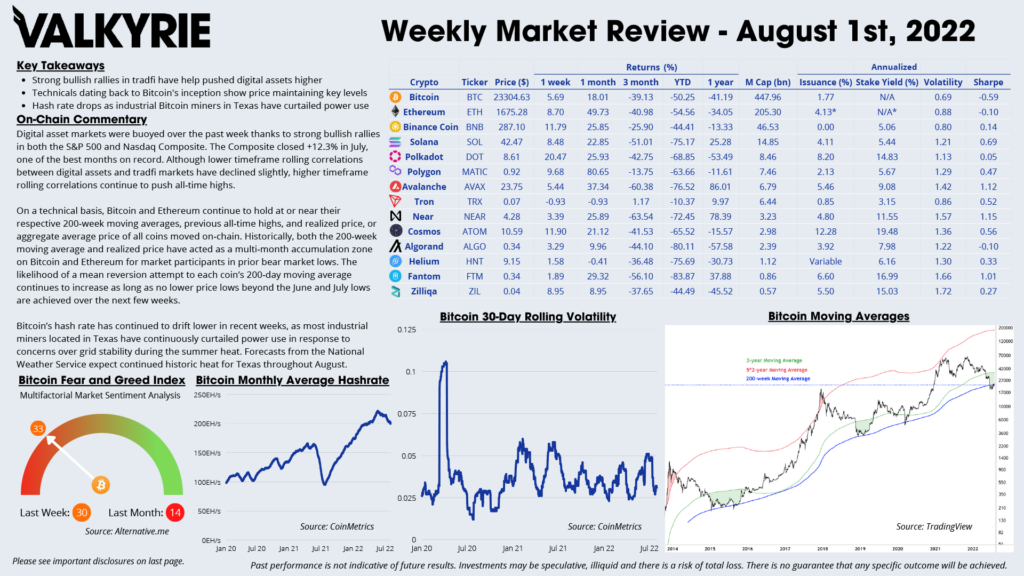

Key Takeaways

- Strong bullish rallies in tradfi have help pushed digital assets higher

- Technicals dating back to Bitcoin’s inception show price maintaining key levels

- Hash rate drops as industrial Bitcoin miners in Texas have curtailed power use

Digital asset markets were buoyed over the past week thanks to strong bullish rallies in both the S&P 500 and Nasdaq Composite. The Composite closed +12.3% in July, one of the best months on record. Although lower timeframe rolling correlations between digital assets and tradfi markets have declined slightly, higher timeframe rolling correlations continue to push all-time highs.

On a technical basis, Bitcoin and Ethereum continue to hold at or near their respective 200-week moving averages, previous all-time highs, and realized price, or aggregate average price of all coins moved on-chain. Historically, both the 200-week moving average and realized price have acted as a multi-month accumulation zone on Bitcoin and Ethereum for market participants in prior bear market lows. The likelihood of a mean reversion attempt to each coin’s 200-day moving average continues to increase as long as no lower price lows beyond the June and July lows are achieved over the next few weeks.

Bitcoin’s hash rate has continued to drift lower in recent weeks, as most industrial miners located in Texas have continuously curtailed power use in response to concerns over grid stability during the summer heat. Forecasts from the National Weather Service expect continued historic heat for Texas throughout August.

Download the Full Weekly Market Review Here

The Portfolio Management Team

Steven McClurg, CIO

Bill Cannon, Portfolio Manager

Wes Cowan, Portfolio Manager, Head of Defi

Josh Olszewicz, Head of Research

Sean Rooney, VP Research and Trading

Will McDonough, Vice Chairman, Investment Committee

Leah Wald, CEO, Investment Committee

Shannon Smith, Head of Investor Relations