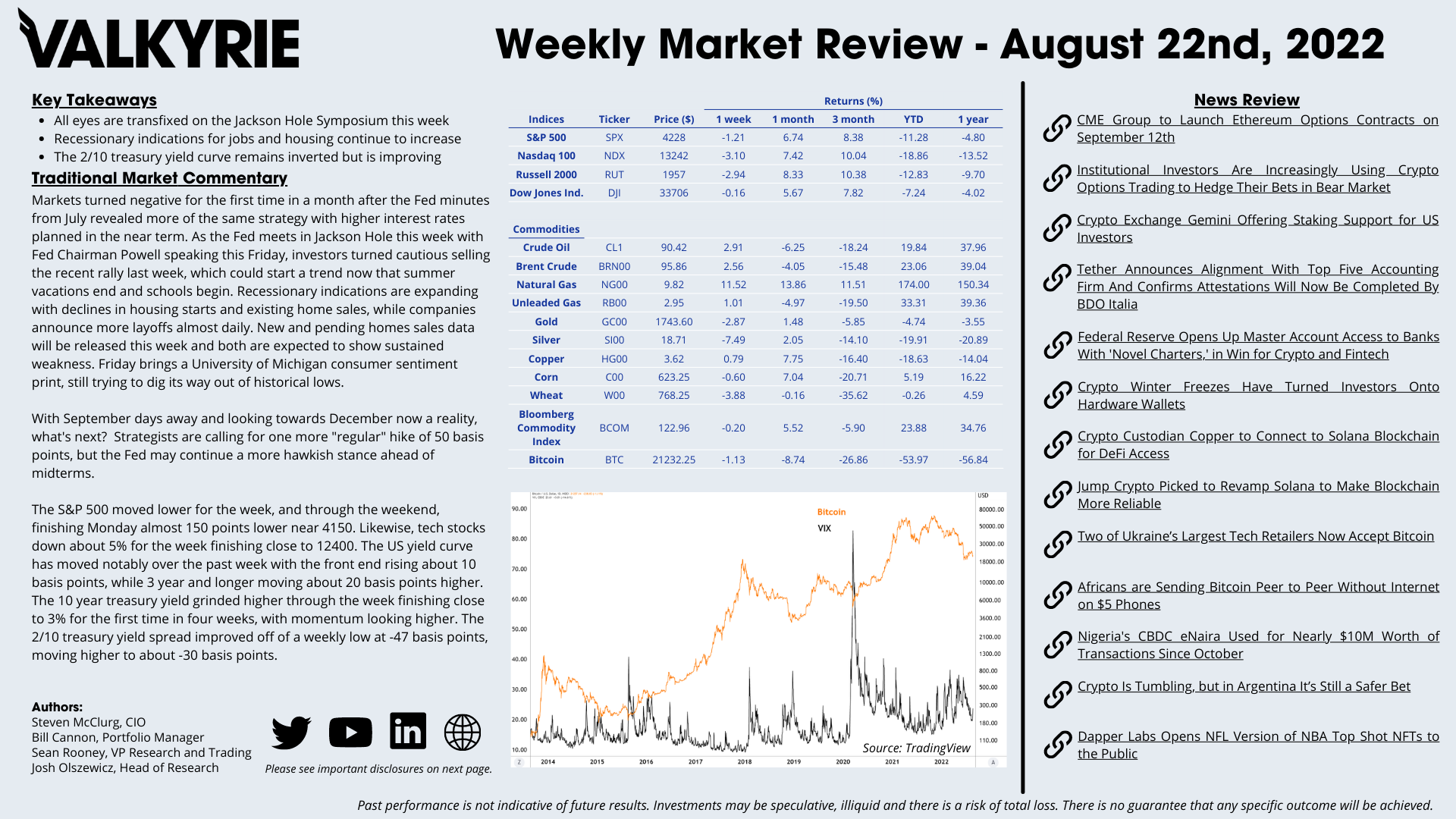

Traditional Market Commentary

Key Takeaways

- All eyes are transfixed on the Jackson Hole Symposium this week

- Recessionary indications for jobs and housing continue to increase

- The 2/10 treasury yield curve remains inverted but is improving

Markets turned negative for the first time in a month after the Fed minutes from July revealed more of the same strategy with higher interest rates planned in the near term. As the Fed meets in Jackson Hole this week with Fed Chairman Powell speaking this Friday, investors turned cautious selling the recent rally last week, which could start a trend now that summer vacations end and schools begin. Recessionary indications are expanding with declines in housing starts and existing home sales, while companies announce more layoffs almost daily. New and pending homes sales data will be released this week and both are expected to show sustained weakness. Friday brings a University of Michigan consumer sentiment print, still trying to dig its way out of historical lows.

With September days away and looking towards December now a reality, what’s next? Strategists are calling for one more “regular” hike of 50 basis points, but the Fed may continue a more hawkish stance ahead of midterms.

The S&P 500 moved lower for the week, and through the weekend, finishing Monday almost 150 points lower near 4150. Likewise, tech stocks down about 5% for the week finishing close to 12400. The US yield curve has moved notably over the past week with the front end rising about 10 basis points, while 3 year and longer moving about 20 basis points higher. The 10 year treasury yield grinded higher through the week finishing close to 3% for the first time in four weeks, with momentum looking higher. The 2/10 treasury yield spread improved off of a weekly low at -47 basis points, moving higher to about -30 basis points.

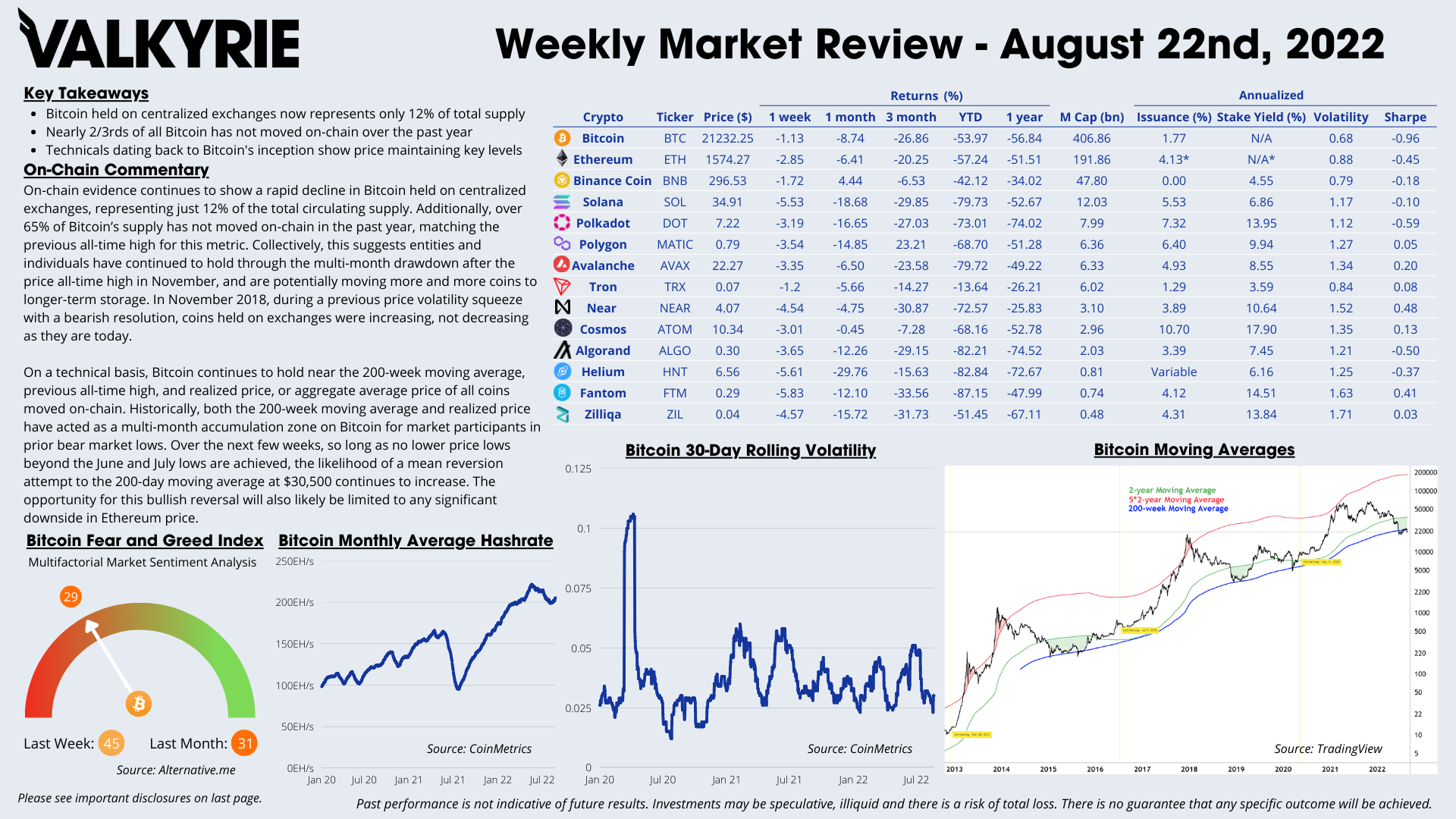

On-Chain Commentary

Key Takeaways

- Bitcoin held on centralized exchanges now represents only 12% of total supply

- Nearly 2/3rds of all Bitcoin has not moved on-chain over the past year

- Technicals dating back to Bitcoin’s inception show price maintaining key levels

On-chain evidence continues to show a rapid decline in Bitcoin held on centralized exchanges, representing just 12% of the total circulating supply. Additionally, over 65% of Bitcoin’s supply has not moved on-chain in the past year, matching the previous all-time high for this metric. Collectively, this suggests entities and individuals have continued to hold through the multi-month drawdown after the price all-time high in November, and are potentially moving more and more coins to longer-term storage. In November 2018, during a previous price volatility squeeze with a bearish resolution, coins held on exchanges were increasing, not decreasing as they are today.

On a technical basis, Bitcoin continues to hold near the 200-week moving average, previous all-time high, and realized price, or aggregate average price of all coins moved on-chain. Historically, both the 200-week moving average and realized price have acted as a multi-month accumulation zone on Bitcoin for market participants in prior bear market lows. Over the next few weeks, so long as no lower price lows beyond the June and July lows are achieved, the likelihood of a mean reversion attempt to the 200-day moving average at $30,500 continues to increase. The opportunity for this bullish reversal will also likely be limited to any significant downside in Ethereum price.

Download the Full Weekly Market Review Here