Calm Before the Real Storm

Week of March 7th, 2022

We have been warning about higher inflation and higher commodity prices for over two years. These price increases are a result of loose monetary policy and high governmental spending. But oftentimes, it takes an event for prices to realize their new fair value, though sometimes the event will drive the pendulum past center in the process.

Oil and Wheat are the two most important commodities to watch right now, as any supply chain disruptions in Europe will continue to push prices higher in the rest of the world for most other commodities. Economic indicators continue to build the story on the inflation strategy as the reported unemployment rate declined Friday to 3.8% from 4.0% last month, in addition to change in non-farm payrolls rising by 678,000, well above the survey of 467,000. Fed Chairman Jerome Powell has already indicated a proposal of one 25 basis point increase ahead of the FOMC meeting next week. A rate rise would be the first of the year and has been highly expected for three months now. The year over year Consumer Price Index will be released on March 10th and is surveyed to increase to 7.8% from 7.5% last month. CPI was 7.0% at the end of 2021. CPI excluding food and energy is surveyed to rise to 6.4%, up from 6.0% last month and up from 5.5% at the end of last year. These will be the last major indicators for the Fed to consider before their two day meeting begins on March 15th.

Despite the volatility over the past couple weeks, U.S. equity markets have been surprisingly stable following the initial Russian attack on the evening of February 23rd. The S&P 500 index is about unchanged since February 23rd, with the VIX currently at the high end of the current range between 28 and 34. For reference, the S&P remains down about 10% year to date, but support at this current level has been relevant ahead of next week’s Fed meeting. The Nasdaq Composite is currently down about 2% during the same period, with the technology driven index down about 16% year to date. After a couple moments of eclipsing the 2% level last month, the 10 year treasury yield is now at 1.75%, down about 25 basis points since the start of the war. Bitcoin is higher about 5% during this period, but still down about 15% year to date.

On-Chain Update

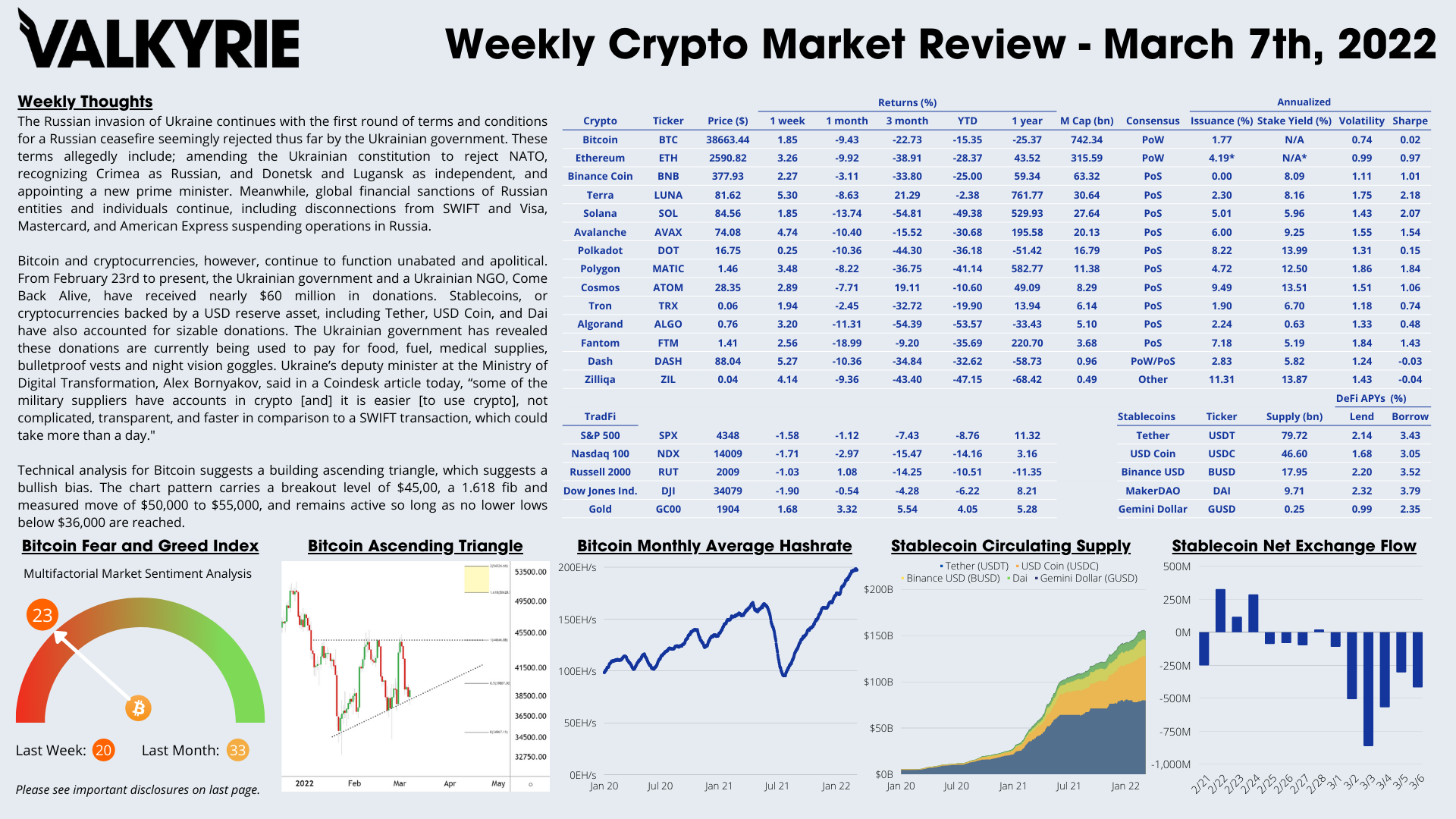

The Russian invasion of Ukraine continues with the first round of terms and conditions for a Russian ceasefire seemingly rejected thus far by the Ukrainian government. These terms allegedly include; amending the Ukrainian constitution to reject NATO, recognizing Crimea as Russian, and Donetsk and Lugansk as independent, and appointing a new prime minister. Meanwhile, global financial sanctions of Russian entities and individuals continue, including disconnections from SWIFT and suspension of operations of Visa, Mastercard, and American Express.

Bitcoin and cryptocurrencies, however, continue to function unabated and apolitical. From February 23rd to present, the Ukrainian government and a Ukrainian NGO, Come Back Alive, have received nearly $60 million in donations. Stablecoins, or cryptocurrencies backed by a USD reserve asset, including Tether, USD Coin, and Dai have also accounted for sizable donations. The Ukrainian government has revealed these donations are currently being used to pay for food, fuel, medical supplies, bulletproof vests and night vision goggles. Ukraine’s deputy minister at the Ministry of Digital Transformation, Alex Bornyakov, said in a Coindesk article today, “some of the military suppliers have accounts in crypto [and] it is easier [to use crypto], not complicated, transparent, and faster in comparison to a SWIFT transaction, which could take more than a day,” he said.

Technical analysis for bitcoin suggests a building ascending triangle, which carries a bullish bias. The chart pattern carries a 1.618 fib and measured move of $50,000 to $55,000 and remains active so long as no lower lows below $36,000 are reached.

Download the Full Weekly Market Review Here

The Portfolio Management Team

Steven McClurg, CIO

Bill Cannon, Portfolio Manager

Wes Cowan, Portfolio Manager, Head of Defi

Josh Olszewicz, Head of Research

Sean Rooney, VP Research and Trading

Will McDonough, Vice Chairman, Investment Committee

Leah Wald, CEO, Investment Committee

Shannon Smith, Head of Investor Relations