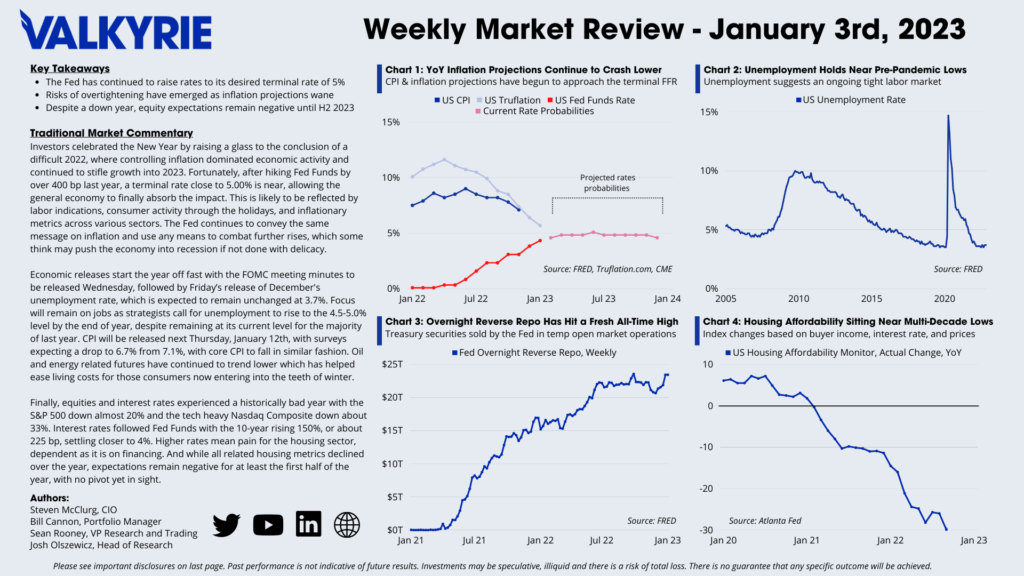

Traditional Market Commentary

- The Fed has continued to raise rates to its desired terminal rate of 5%

- Risks of overtightening have emerged as inflation projections wane

- Despite a down year, equity expectations remain negative until H2 2023

Investors celebrated the New Year by raising a glass to the conclusion of a difficult 2022, where controlling inflation dominated economic activity and continued to stifle growth into 2023. Fortunately, after hiking Fed Funds by over 400 bp last year, a terminal rate close to 5.00% is near, allowing the general economy to finally absorb the impact. This is likely to be reflected by labor indications, consumer activity through the holidays, and inflationary metrics across various sectors. The Fed continues to convey the same message on inflation and use any means to combat further rises, which some think may push the economy into recession if not done with delicacy.

Economic releases start the year off fast with the FOMC meeting minutes to be released Wednesday, followed by Friday’s release of December’s unemployment rate, which is expected to remain unchanged at 3.7%. Focus will remain on jobs as strategists call for unemployment to rise to the 4.5-5.0% level by the end of year, despite remaining at its current level for the majority of last year. CPI will be released next Thursday, January 12th, with surveys expecting a drop to 6.7% from 7.1%, with core CPI to fall in similar fashion. Oil and energy related futures have continued to trend lower which has helped ease living costs for those consumers now entering into the teeth of winter.

Finally, equities and interest rates experienced a historically bad year with the S&P 500 down almost 20% and the tech heavy Nasdaq Composite down about 33%. Interest rates followed Fed Funds with the 10-year rising 150%, or about 225 bp, settling closer to 4%. Higher rates mean pain for the housing sector, dependent as it is on financing. And while all related housing metrics declined over the year, expectations remain negative for at least the first half of the year, with no pivot yet in sight.

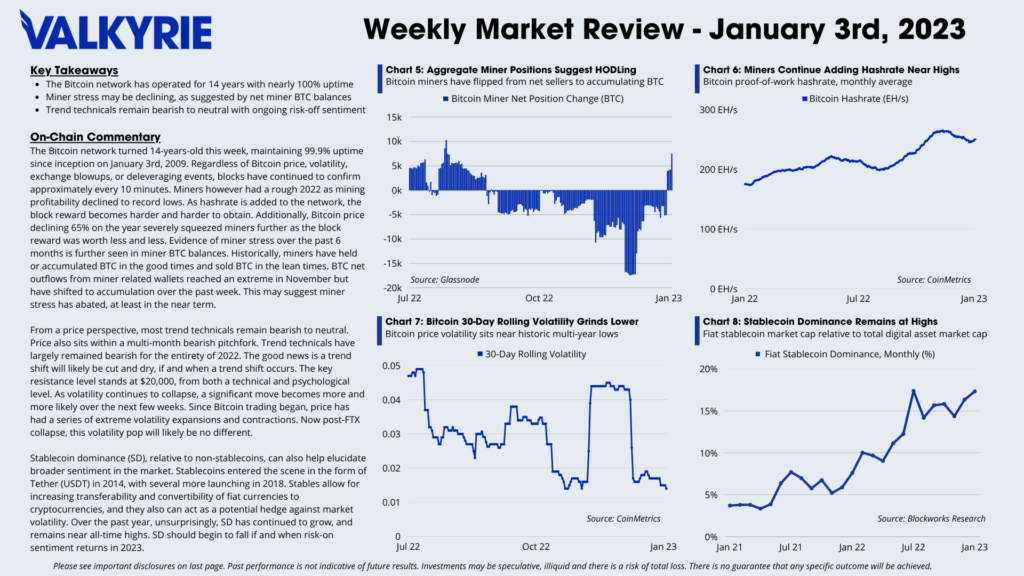

On-Chain Commentary

- The Bitcoin network has operated for 14 years with nearly 100% uptime

- Miner stress may be declining, as suggested by net miner BTC balances

- Trend technicals remain bearish to neutral with ongoing risk-off sentiment

The Bitcoin network turned 14-years-old this week, maintaining 99.9% uptime since inception on January 3rd, 2009. Regardless of Bitcoin price, volatility, exchange blowups, or deleveraging events, blocks have continued to confirm approximately every 10 minutes. Miners however had a rough 2022 as mining profitability declined to record lows. As hashrate is added to the network, the block reward becomes harder and harder to obtain. Additionally, Bitcoin price declining 65% on the year severely squeezed miners further as the block reward was worth less and less. Evidence of miner stress over the past 6 months is further seen in miner BTC balances. Historically, miners have held or accumulated BTC in the good times and sold BTC in the lean times. BTC net outflows from miner related wallets reached an extreme in November but have shifted to accumulation over the past week. This may suggest miner stress has abated, at least in the near term.

From a price perspective, most trend technicals remain bearish to neutral. Price also sits within a multi-month bearish pitchfork. Trend technicals have largely remained bearish for the entirety of 2022. The good news is a trend shift will likely be cut and dry, if and when a trend shift occurs. The key resistance level stands at $20,000, from both a technical and psychological level. As volatility continues to collapse, a significant move becomes more and more likely over the next few weeks. Since Bitcoin trading began, price has had a series of extreme volatility expansions and contractions. Now post-FTX collapse, this volatility pop will likely be no different.

Stablecoin dominance (SD), relative to non-stablecoins, can also help elucidate broader sentiment in the market. Stablecoins entered the scene in the form of Tether (USDT) in 2014, with several more launching in 2018. Stables allow for increasing transferability and convertibility of fiat currencies to cryptocurrencies, and they also can act as a potential hedge against market volatility. Over the past year, unsurprisingly, SD has continued to grow, and remains near all-time highs. SD should begin to fall if and when risk-on sentiment returns in 2023.