Traditional Market Commentary

- Optimistic rallies continue as sentiment shifts towards a less hawkish Fed

- Earnings season has been most punishing towards the tech sector

- The Fed may soon adjust a new normal for inflation targets above 2.0%

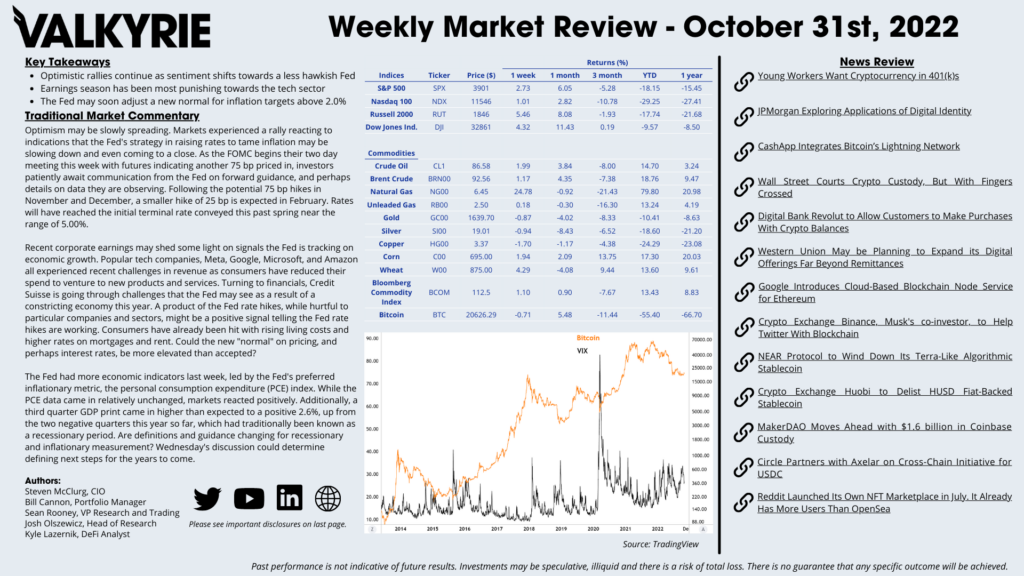

Optimism may be slowly spreading. Markets experienced a rally reacting to indications that the Fed’s strategy in raising rates to tame inflation may be slowing down and even coming to a close. As the FOMC begins their two day meeting this week with futures indicating another 75 bp priced in, investors patiently await communication from the Fed on forward guidance, and perhaps details on data they are observing. Following the potential 75 bp hikes in November and December, a smaller hike of 25 bp is expected in February. Rates will have reached the initial terminal rate conveyed this past spring near the range of 5.00%.

Recent corporate earnings may shed some light on signals the Fed is tracking on economic growth. Popular tech companies, Meta, Google, Microsoft, and Amazon all experienced recent challenges in revenue as consumers have reduced their spend to venture to new products and services. Turning to financials, Credit Suisse is going through challenges that the Fed may see as a result of a constricting economy this year. A product of the Fed rate hikes, while hurtful to particular companies and sectors, might be a positive signal telling the Fed rate hikes are working. Consumers have already been hit with rising living costs and higher rates on mortgages and rent. Could the new “normal” on pricing, and perhaps interest rates, be more elevated than accepted?

The Fed had more economic indicators last week, led by the Fed’s preferred inflationary metric, the personal consumption expenditure (PCE) index. While the PCE data came in relatively unchanged, markets reacted positively. Additionally, a third quarter GDP print came in higher than expected to a positive 2.6%, up from the two negative quarters this year so far, which had traditionally been known as a recessionary period. Are definitions and guidance changing for recessionary and inflationary measurement? Wednesday’s discussion could determine defining next steps for the years to come.

On-Chain Commentary

- Satoshi Nakamoto released the Bitcoin white paper 14 years ago today

- The decentralized network has had nearly 100% uptime since launching in 2009

- Bitcoin and other digital assets have begun experiencing upside volatility

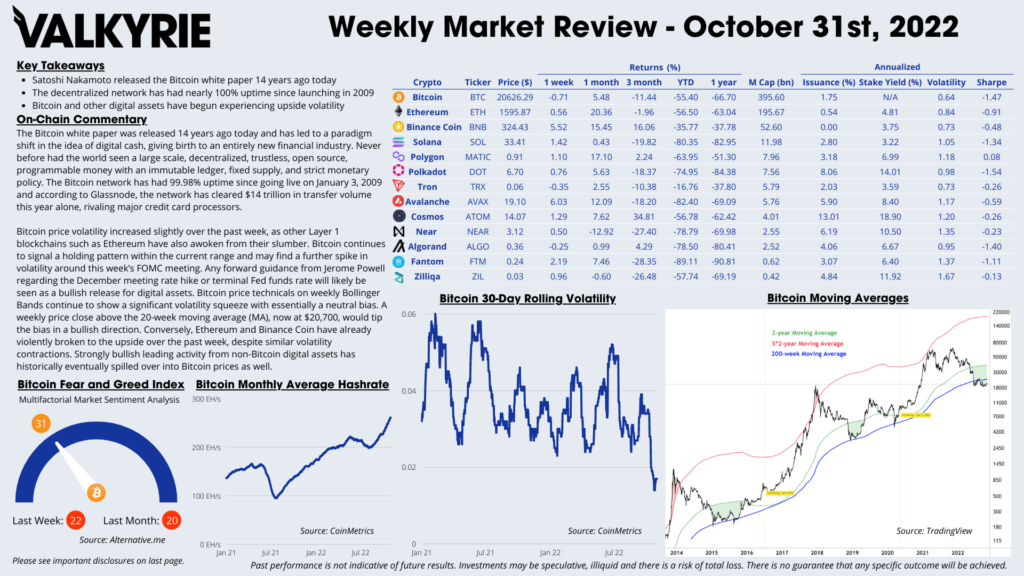

The Bitcoin white paper was released 14 years ago today and has led to a paradigm shift in the idea of digital cash, giving birth to an entirely new financial industry. Never before had the world seen a large scale, decentralized, trustless, open source, programmable money with an immutable ledger, fixed supply, and strict monetary policy. The Bitcoin network has had 99.98% uptime since going live on January 3, 2009 and according to Glassnode, the network has cleared $14 trillion in transfer volume this year alone, rivaling major credit card processors.

Bitcoin price volatility increased slightly over the past week, as other Layer 1 blockchains such as Ethereum have also awoken from their slumber. Bitcoin continues to signal a holding pattern within the current range and may find a further spike in volatility around this week’s FOMC meeting. Any forward guidance from Jerome Powell regarding the December meeting rate hike or terminal Fed funds rate will likely be seen as a bullish release for digital assets. Bitcoin price technicals on weekly Bollinger Bands continue to show a significant volatility squeeze with essentially a neutral bias. A weekly price close above the 20-week moving average (MA), now at $20,700, would tip the bias in a bullish direction. Conversely, Ethereum and Binance Coin have already violently broken to the upside over the past week, despite similar volatility contractions. Strongly bullish leading activity from non-Bitcoin digital assets has historically eventually spilled over into Bitcoin prices as well.