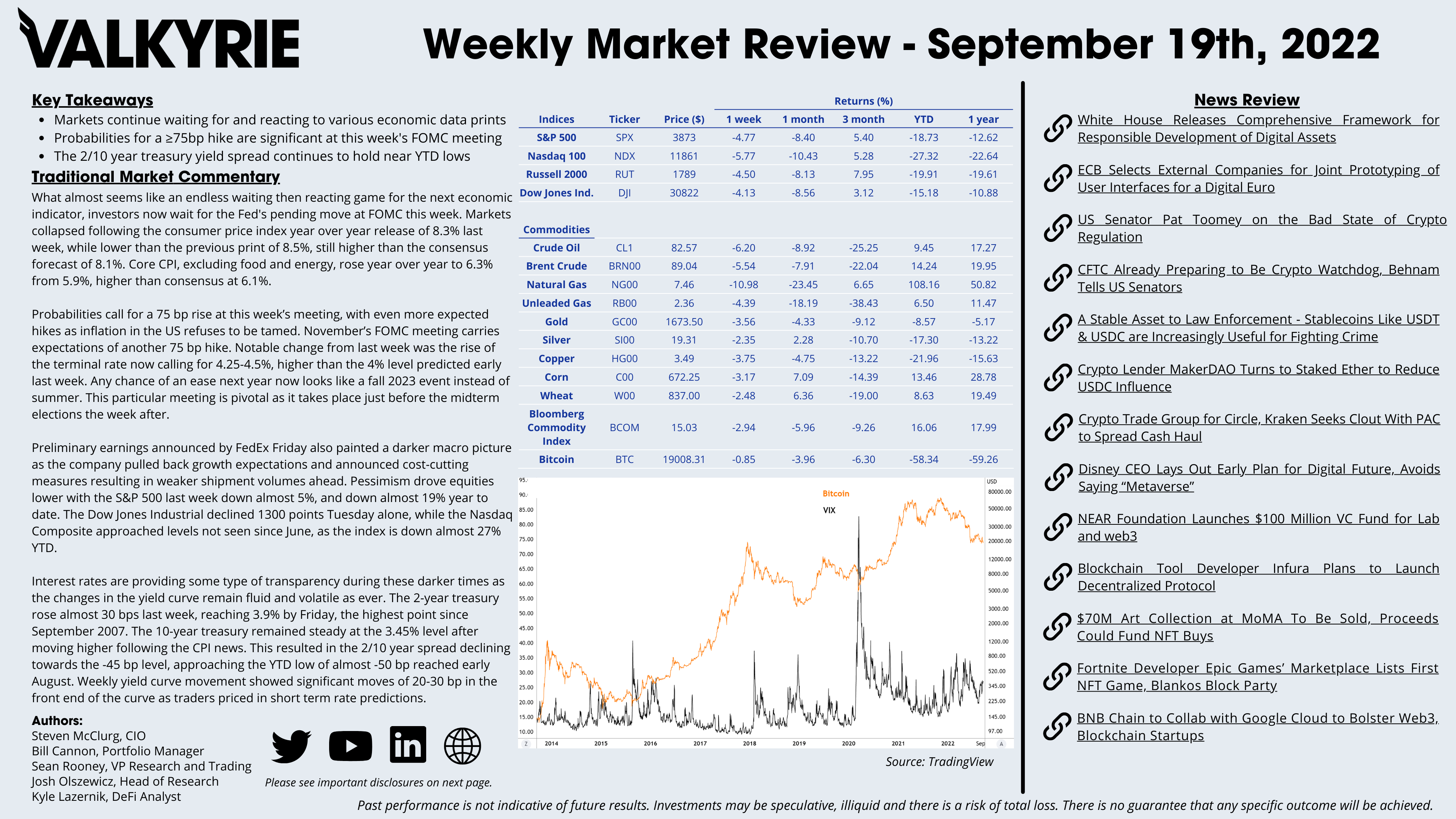

Traditional Market Commentary

- Markets continue waiting for and reacting to various economic data prints

- Probabilities for a ≥75bp hike are significant at this week’s FOMC meeting

- The 2/10 year treasury yield spread continues to hold near YTD lows

What almost seems like an endless waiting then reacting game for the next economic indicator, investors now wait for the Fed’s pending move at FOMC this week. Markets collapsed following the consumer price index year over year release of 8.3% last week, while lower than the previous print of 8.5%, still higher than the consensus forecast of 8.1%. Core CPI, excluding food and energy, rose year over year to 6.3% from 5.9%, higher than consensus at 6.1%.

Probabilities call for a 75 bp rise at this week’s meeting, with even more expected hikes as inflation in the US refuses to be tamed. November’s FOMC meeting carries expectations of another 75 bp hike. Notable change from last week was the rise of the terminal rate now calling for 4.25-4.5%, higher than the 4% level predicted early last week. Any chance of an ease next year now looks like a fall 2023 event instead of summer. This particular meeting is pivotal as it takes place just before the midterm elections the week after.

Preliminary earnings announced by FedEx Friday also painted a darker macro picture as the company pulled back growth expectations and announced cost-cutting measures resulting in weaker shipment volumes ahead. Pessimism drove equities lower with the S&P 500 last week down almost 5%, and down almost 19% year to date. The Dow Jones Industrial declined 1300 points Tuesday alone, while the Nasdaq Composite approached levels not seen since June, as the index is down almost 27% YTD.

Interest rates are providing some type of transparency during these darker times as the changes in the yield curve remain fluid and volatile as ever. The 2-year treasury rose almost 30 bps last week, reaching 3.9% by Friday, the highest point since September 2007. The 10-year treasury remained steady at the 3.45% level after moving higher following the CPI news. This resulted in the 2/10 year spread declining towards the -45 bp level, approaching the YTD low of almost -50 bp reached early August. Weekly yield curve movement showed significant moves of 20-30 bp in the front end of the curve as traders priced in short term rate predictions.

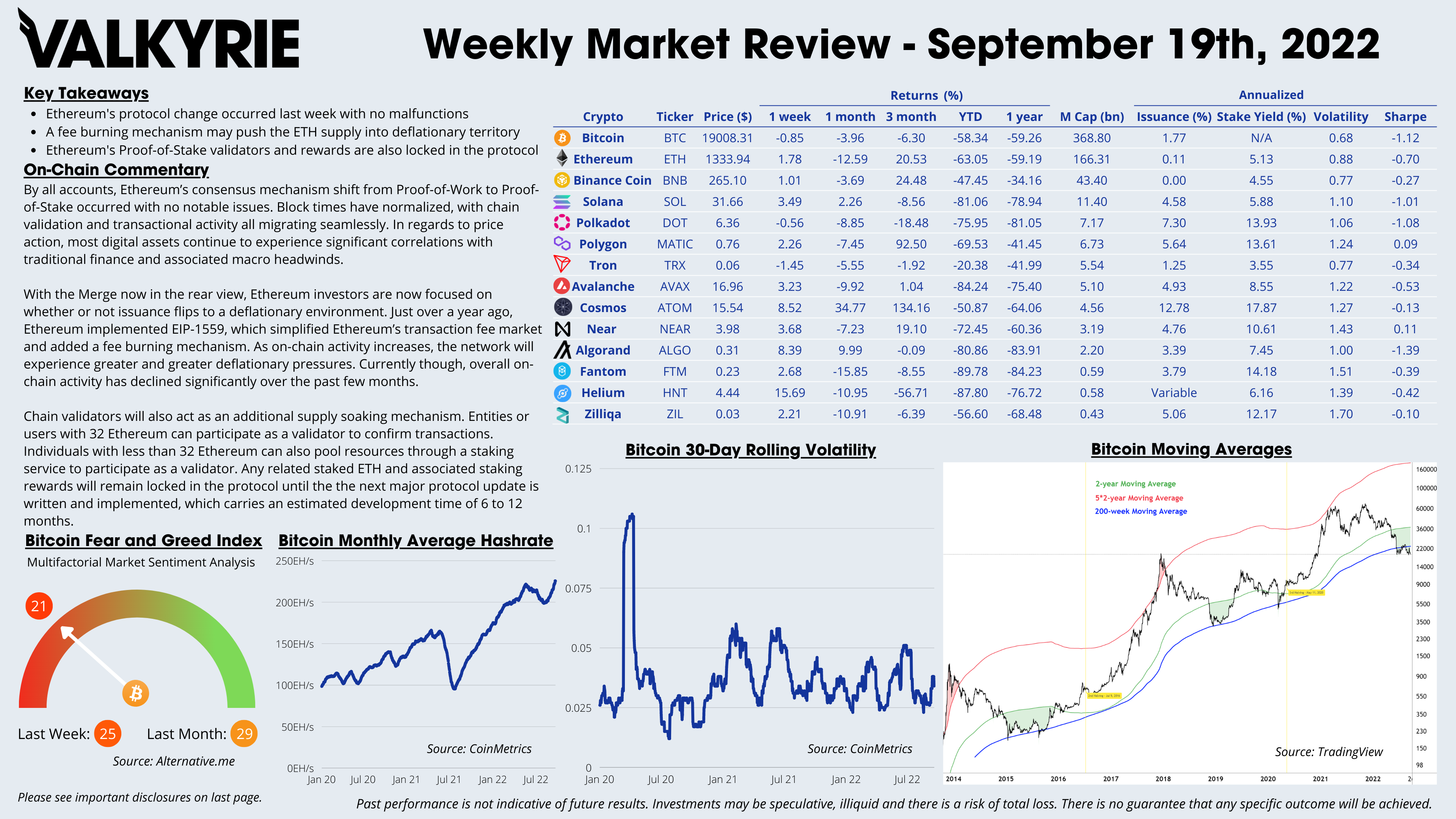

On-Chain Commentary

- Ethereum’s protocol change occurred last week with no malfunctions

- A fee burning mechanism may push the ETH supply into deflationary territory

- Ethereum’s Proof-of-Stake validators and rewards are also locked in the protocol

By all accounts, Ethereum’s consensus mechanism shift from Proof-of-Work to Proof-of-Stake occurred with no notable issues. Block times have normalized, with chain validation and transactional activity all migrating seamlessly. In regards to price action, most digital assets continue to experience significant correlations with traditional finance and associated macro headwinds.

With the Merge now in the rear view, Ethereum investors are now focused on whether or not issuance flips to a deflationary environment. Just over a year ago, Ethereum implemented EIP-1559, which simplified Ethereum’s transaction fee market and added a fee burning mechanism. As on-chain activity increases, the network will experience greater and greater deflationary pressures. Currently though, overall on-chain activity has declined significantly over the past few months.

Chain validators will also act as an additional supply soaking mechanism. Entities or users with 32 Ethereum can participate as a validator to confirm transactions. Individuals with less than 32 Ethereum can also pool resources through a staking service to participate as a validator. Any related staked ETH and associated staking rewards will remain locked in the protocol until the the next major protocol update is written and implemented, which carries an estimated development time of 6 to 12 months.

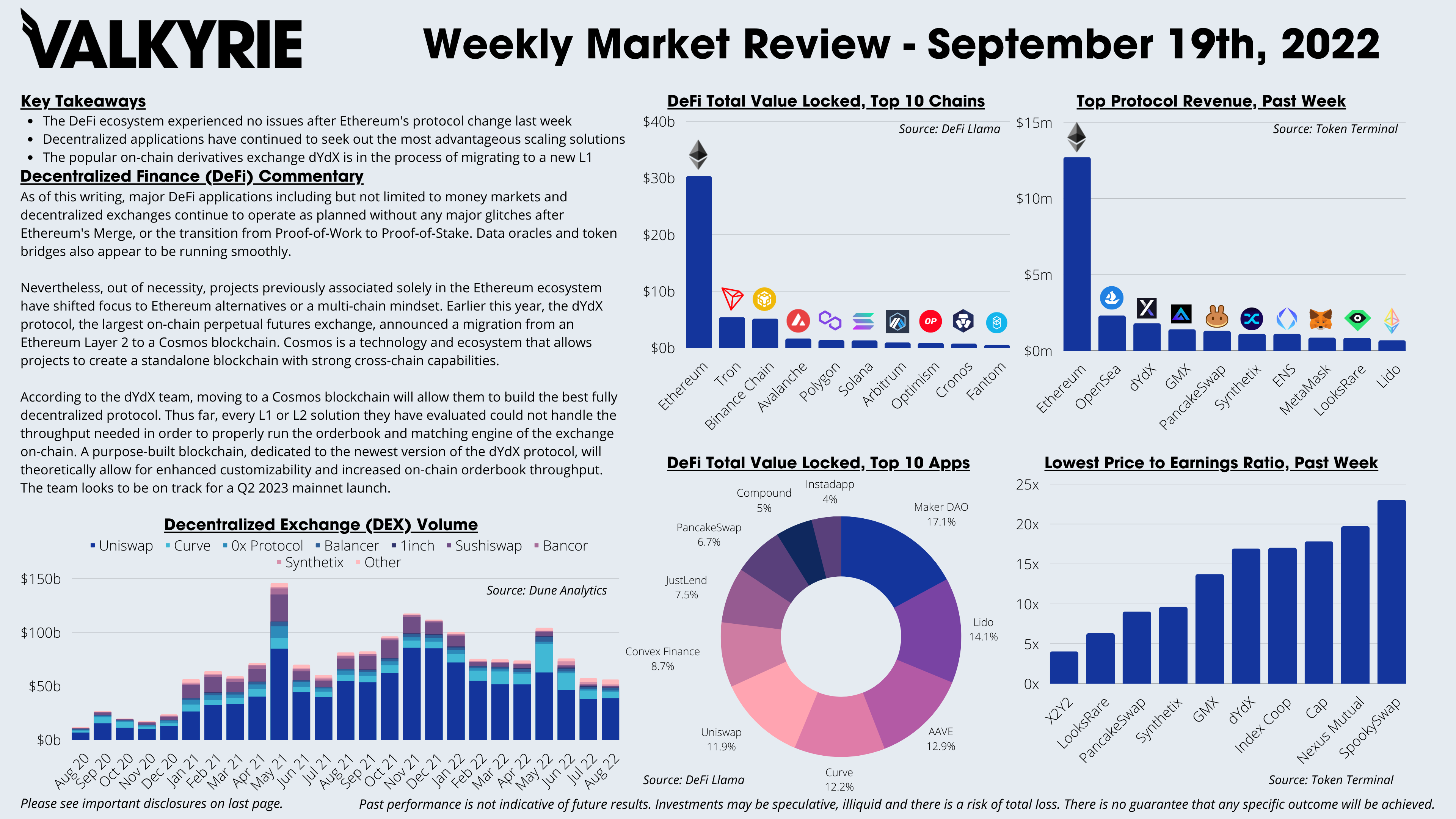

DeFi Commentary

- The DeFi ecosystem experienced no issues after Ethereum’s protocol change last week

- Decentralized applications have continued to seek out the most advantageous scaling solutions

- The popular on-chain derivatives exchange dYdX is in the process of migrating to a new L1

As of this writing, major DeFi applications including but not limited to money markets and decentralized exchanges continue to operate as planned without any major glitches after Ethereum’s Merge, or the transition from Proof-of-Work to Proof-of-Stake. Data oracles and token bridges also appear to be running smoothly.

Nevertheless, out of necessity, projects previously associated solely in the Ethereum ecosystem have shifted focus to Ethereum alternatives or a multi-chain mindset. Earlier this year, the dYdX protocol, the largest on-chain perpetual futures exchange, announced a migration from an Ethereum Layer 2 to a Cosmos blockchain. Cosmos is a technology and ecosystem that allows projects to create a standalone blockchain with strong cross-chain capabilities.

According to the dYdX team, moving to a Cosmos blockchain will allow them to build the best fully decentralized protocol. Thus far, every L1 or L2 solution they have evaluated could not handle the throughput needed in order to properly run the orderbook and matching engine of the exchange on-chain. A purpose-built blockchain, dedicated to the newest version of the dYdX protocol, will theoretically allow for enhanced customizability and increased on-chain orderbook throughput. The team looks to be on track for a Q2 2023 mainnet launch.

Download the Full Weekly Market Review Here