Traditional Market Commentary

- Inflation has begun to fall but remains well above the Fed’s 2% target

- The Fed announced a 50 bp rate hike last week, w/smaller hikes expected

- PCE and housing data released this week are expected to move lower

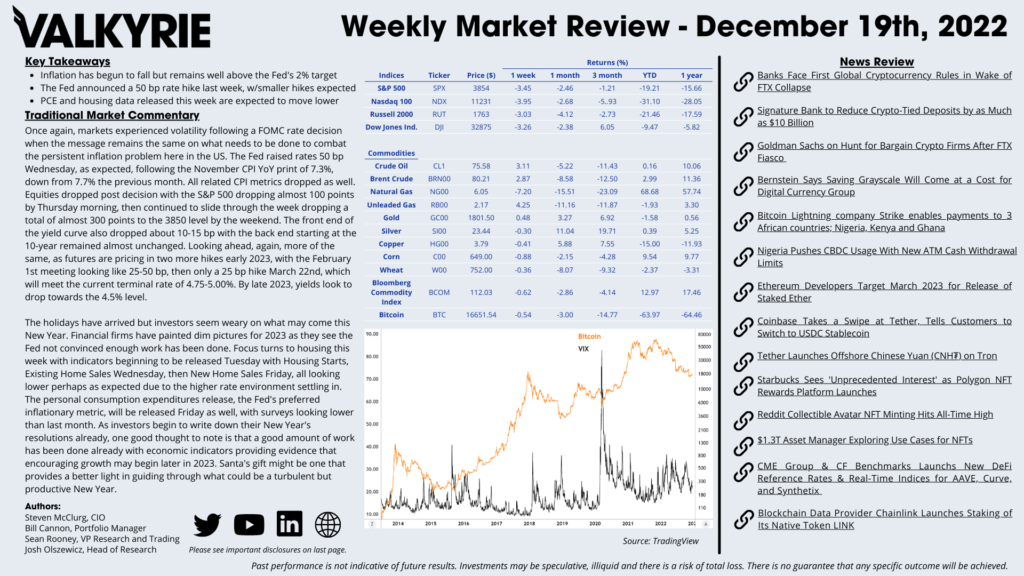

Once again, markets experienced volatility following a FOMC rate decision when the message remains the same on what needs to be done to combat the persistent inflation problem here in the US. The Fed raised rates 50 bp Wednesday, as expected, following the November CPI YoY print of 7.3%, down from 7.7% the previous month. All related CPI metrics dropped as well. Equities dropped post decision with the S&P 500 dropping almost 100 points by Thursday morning, then continued to slide through the week dropping a total of almost 300 points to the 3850 level by the weekend. The front end of the yield curve also dropped about 10-15 bp with the back end starting at the 10-year remained almost unchanged. Looking ahead, again, more of the same, as futures are pricing in two more hikes early 2023, with the February 1st meeting looking like 25-50 bp, then only a 25 bp hike March 22nd, which will meet the current terminal rate of 4.75-5.00%. By late 2023, yields look to drop towards the 4.5% level.

The holidays have arrived but investors seem weary on what may come this New Year. Financial firms have painted dim pictures for 2023 as they see the Fed not convinced enough work has been done. Focus turns to housing this week with indicators beginning to be released Tuesday with Housing Starts, Existing Home Sales Wednesday, then New Home Sales Friday, all looking lower perhaps as expected due to the higher rate environment settling in. The personal consumption expenditures release, the Fed’s preferred inflationary metric, will be released Friday as well, with surveys looking lower than last month. As investors begin to write down their New Year’s resolutions already, one good thought to note is that a good amount of work has been done already with economic indicators providing evidence that encouraging growth may begin later in 2023. Santa’s gift might be one that provides a better light in guiding through what could be a turbulent but productive New Year.

On-Chain Commentary

- 2022 was marred by fake yields, significant leverage, and rehypothecation

- Bitcoin & other digital assets continue to function, unperturbed by 2022’s events

- Use cases should continue to expand & strengthen throughout 2023 & beyond

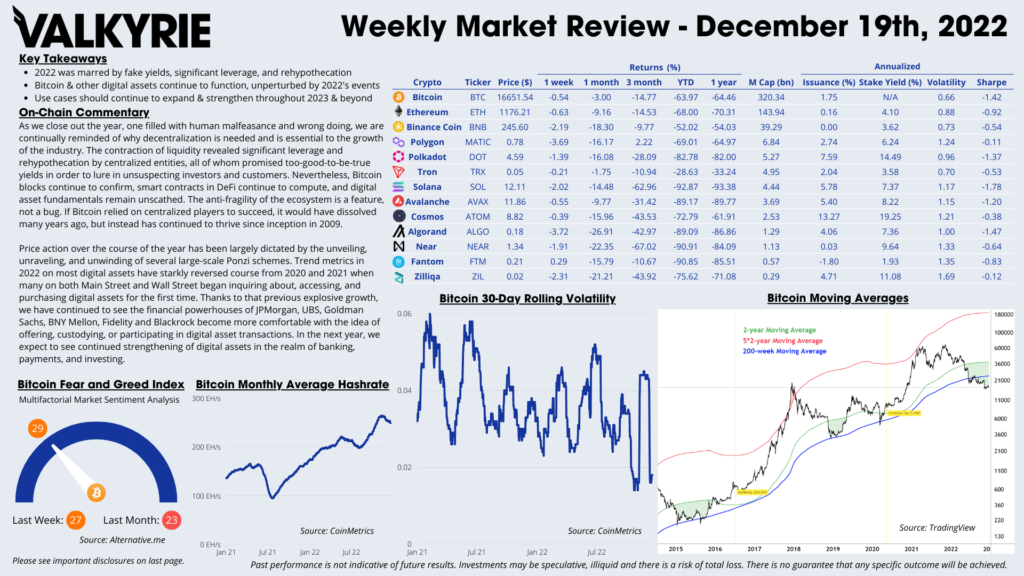

As we close out the year, one filled with human malfeasance and wrong doing, we are continually reminded of why decentralization is needed and is essential to the growth of the industry. The contraction of liquidity revealed significant leverage and rehypothecation by centralized entities, all of whom promised too-good-to-be-true yields in order to lure in unsuspecting investors and customers. Nevertheless, Bitcoin blocks continue to confirm, smart contracts in DeFi continue to compute, and digital asset fundamentals remain unscathed. The anti-fragility of the ecosystem is a feature, not a bug. If Bitcoin relied on centralized players to succeed, it would have dissolved many years ago, but instead has continued to thrive since inception in 2009.

Price action over the course of the year has been largely dictated by the unveiling, unraveling, and unwinding of several large-scale Ponzi schemes. Trend metrics in 2022 on most digital assets have starkly reversed course from 2020 and 2021 when many on both Main Street and Wall Street began inquiring about, accessing, and purchasing digital assets for the first time. Thanks to that previous explosive growth, we have continued to see the financial powerhouses of JPMorgan, UBS, Goldman Sachs, BNY Mellon, Fidelity and Blackrock become more comfortable with the idea of offering, custodying, or participating in digital asset transactions. In the next year, we expect to see continued strengthening of digital assets in the realm of banking, payments, and investing.