Traditional Market Commentary

- November’s CPI data will be released tomorrow morning, exp 7.3

- Market probabilities expect a 50bp hike for Wednesday’s FOMC meeting

- The US labor market remains resilient in the face of rising rates

Investors have waited patiently for the last economic indications of the year with the November CPI print to be released Tuesday, then the FOMC rate decision announced Wednesday. As the holiday quickly approaches, it seems as though most are ready to celebrate the new year and find 2022 in the history books as one of the most challenging and frustrating investing years ever. US inflation grew from being a supposed transitory event to a full global situation, especially following the beginning of the Ukrainian-Russian war in February, which tore apart commodity markets and roiled world politics. Fed funds futures have priced in the next 50 bp hike Wednesday, then another 50 bps at the next meeting on February 1st. Post-meeting comments by Fed Chairman Powell look to remain hawkish, but with a slightly calmer tone, as the terminal rate level of 5.00-5.25% is near allowing a more gradual escalation of subsequent rate hikes to get there. Looking towards the new year, futures are pricing in a pivot point near September where rates look to decline and end the year close to 4.5%.

The labor market has remained strong with little change in unemployment and weekly jobless claims, but overall housing has weakened, mainly due to the severe rise in rates and drop in demand over the year. Overall PPI declined last week, while the University of Michigan consumer sentiment improved closer to the 60 index level. What will it take for the Fed to look the other direction? With the terminal rate near the expected 5.00-5.25% range, perhaps the Fed is waiting for final effects of all the rate hikes to materialize and let the medicine take its course. When the adage of economic good news means good news prevails again, the moment of returning the economy to a more stable or near normal environment will come, allowing investors to start finding value across all sectors.

On-Chain Commentary

- Markets continue digesting FTX contagion and waiting for Fed rhetoric on the 14th

- Technicals for BTC & ETH reveal price levels seen in prior bear market periods

- Traders & investors continue to pull coins off of exchanges to self-custody

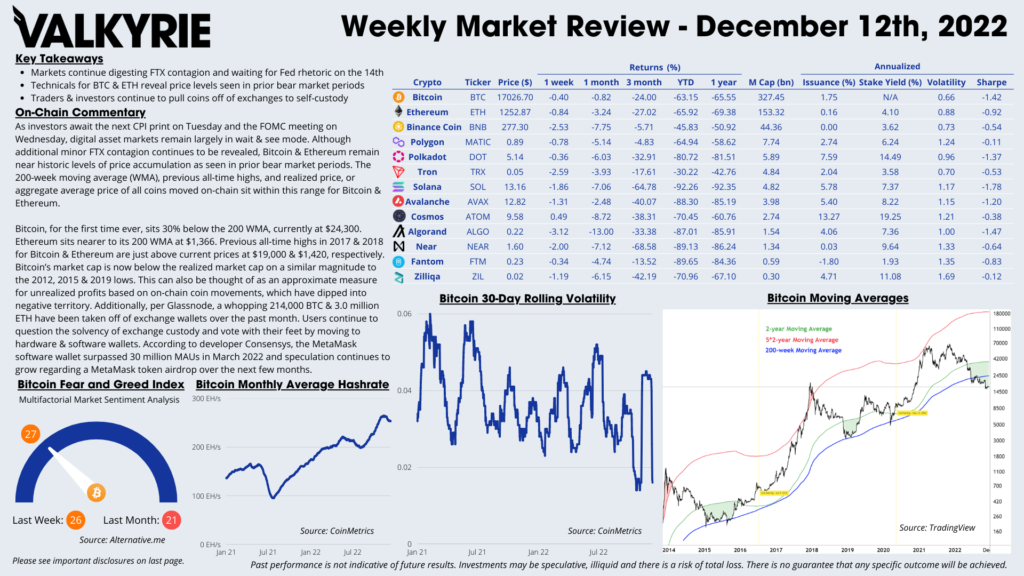

As investors await the next CPI print on Tuesday and the FOMC meeting on Wednesday, digital asset markets remain largely in wait & see mode. Although additional minor FTX contagion continues to be revealed, Bitcoin & Ethereum remain near historic levels of price accumulation as seen in prior bear market periods. The 200-week moving average (WMA), previous all-time highs, and realized price, or aggregate average price of all coins moved on-chain sit within this range for Bitcoin & Ethereum.

Bitcoin, for the first time ever, sits 30% below the 200 WMA, currently at $24,300. Ethereum sits nearer to its 200 WMA at $1,366. Previous all-time highs in 2017 & 2018 for Bitcoin & Ethereum are just above current prices at $19,000 & $1,420, respectively. Bitcoin’s market cap is now below the realized market cap on a similar magnitude to the 2012, 2015 & 2019 lows. This can also be thought of as an approximate measure for unrealized profits based on on-chain coin movements, which have dipped into negative territory. Additionally, per Glassnode, a whopping 214,000 BTC & 3.0 million ETH have been taken off of exchange wallets over the past month. Users continue to question the solvency of exchange custody and vote with their feet by moving to hardware & software wallets. According to developer Consensys, the MetaMask software wallet surpassed 30 million MAUs in March 2022 and speculation continues to grow regarding a MetaMask token airdrop over the next few months.