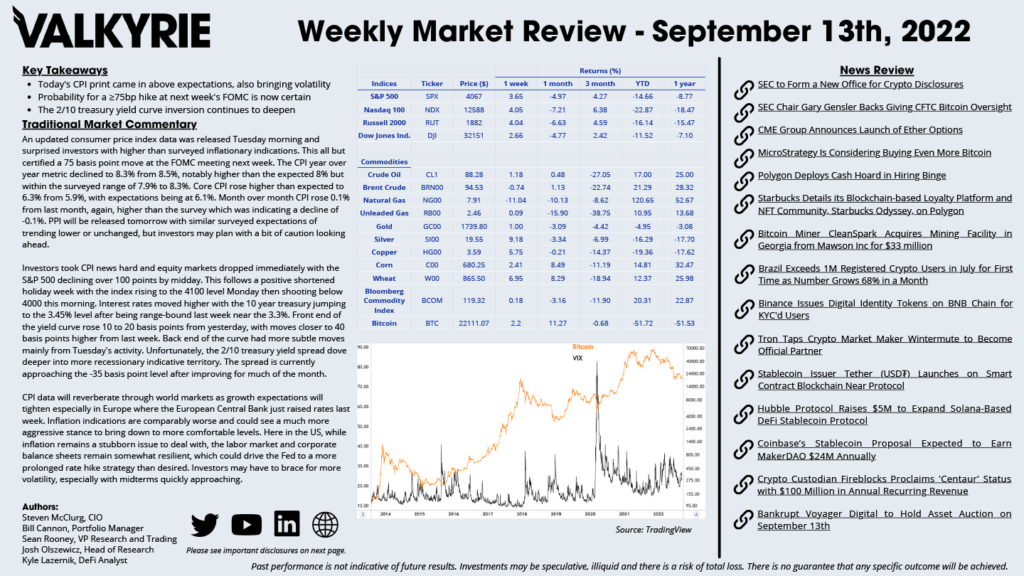

Traditional Market Commentary

- Today’s CPI print came in above expectations, also bringing volatility

- Probability for a ≥75bp hike at next week’s FOMC is now certain

- The 2/10 treasury yield curve inversion continues to deepen

An updated consumer price index data was released Tuesday morning and surprised investors with higher than surveyed inflationary indications. This all but certified a 75 basis point move at the FOMC meeting next week. The CPI year over year metric declined to 8.3% from 8.5%, notably higher than the expected 8% but within the surveyed range of 7.9% to 8.3%. Core CPI rose higher than expected to 6.3% from 5.9%, with expectations being at 6.1%. Month over month CPI rose 0.1% from last month, again, higher than the survey which was indicating a decline of -0.1%. PPI will be released tomorrow with similar surveyed expectations of trending lower or unchanged, but investors may plan with a bit of caution looking ahead.

Investors took CPI news hard and equity markets dropped immediately with the S&P 500 declining over 100 points by midday. This follows a positive shortened holiday week with the index rising to the 4100 level Monday then shooting below 4000 this morning. Interest rates moved higher with the 10 year treasury jumping to the 3.45% level after being range-bound last week near the 3.3%. Front end of the yield curve rose 10 to 20 basis points from yesterday, with moves closer to 40 basis points higher from last week. Back end of the curve had more subtle moves mainly from Tuesday’s activity. Unfortunately, the 2/10 treasury yield spread dove deeper into more recessionary indicative territory. The spread is currently approaching the -35 basis point level after improving for much of the month.

CPI data will reverberate through world markets as growth expectations will tighten especially in Europe where the European Central Bank just raised rates last week. Inflation indications are comparably worse and could see a much more aggressive stance to bring down to more comfortable levels. Here in the US, while inflation remains a stubborn issue to deal with, the labor market and corporate balance sheets remain somewhat resilient, which could drive the Fed to a more prolonged rate hike strategy than desired. Investors may have to brace for more volatility, especially with midterms quickly approaching.

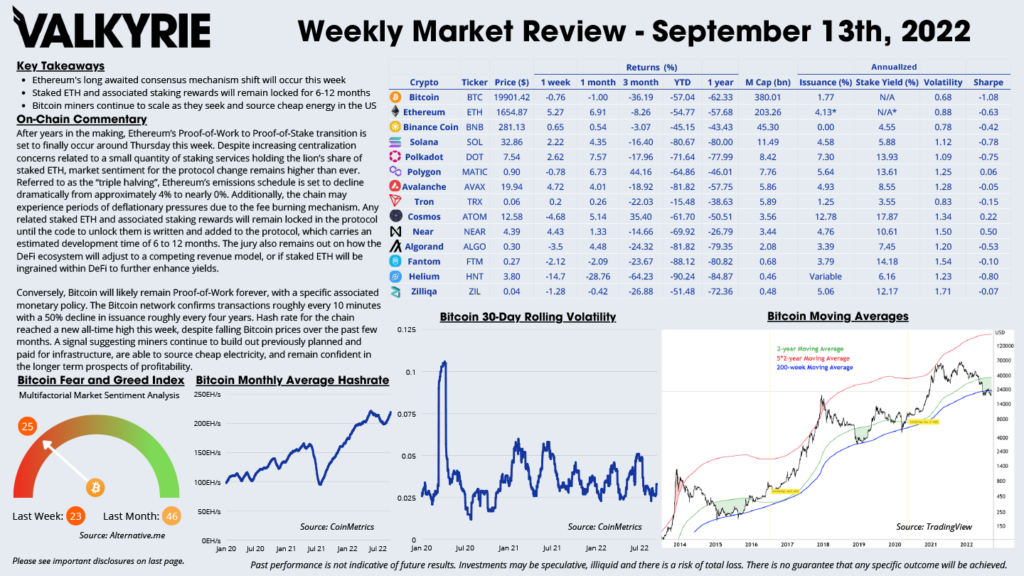

On-Chain Commentary

- Ethereum’s long awaited consensus mechanism shift will occur this week

- Staked ETH and associated staking rewards will remain locked for 6-12 months

- Bitcoin miners continue to scale as they seek and source cheap energy in the US

After years in the making, Ethereum’s Proof-of-Work to Proof-of-Stake transition is set to finally occur around Thursday this week. Despite increasing centralization concerns related to a small quantity of staking services holding the lion’s share of staked ETH, market sentiment for the protocol change remains higher than ever. Referred to as the “triple halving”, Ethereum’s emissions schedule is set to decline dramatically from approximately 4% to nearly 0%. Additionally, the chain may experience periods of deflationary pressures due to the fee burning mechanism. Any related staked ETH and associated staking rewards will remain locked in the protocol until the code to unlock them is written and added to the protocol, which carries an estimated development time of 6 to 12 months. The jury also remains out on how the DeFi ecosystem will adjust to a competing revenue model, or if staked ETH will be ingrained within DeFi to further enhance yields.

Conversely, Bitcoin will likely remain Proof-of-Work forever, with a specific associated monetary policy. The Bitcoin network confirms transactions roughly every 10 minutes with a 50% decline in issuance roughly every four years. Hash rate for the chain reached a new all-time high this week, despite falling Bitcoin prices over the past few months. A signal suggesting miners continue to build out previously planned and paid for infrastructure, are able to source cheap electricity, and remain confident in the longer term prospects of profitability.

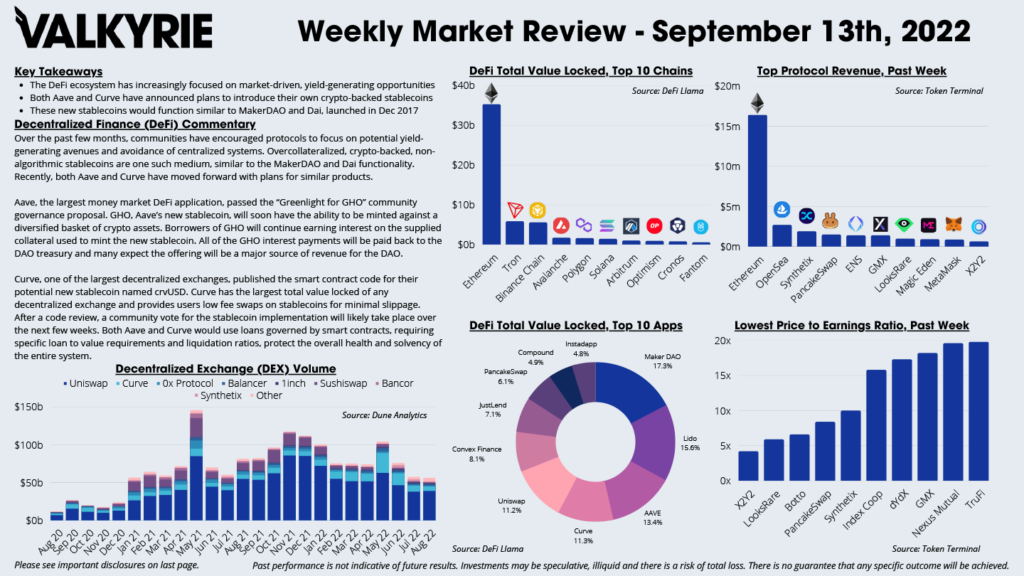

DeFi Commentary

- The DeFi ecosystem has increasingly focused on market-driven, yield-generating opportunities

- Both Aave and Curve have announced plans to introduce their own crypto-backed stablecoins

- These new stablecoins would function similar to MakerDAO and Dai, launched in Dec 2017

Over the past few months, communities have encouraged protocols to focus on potential yield-generating avenues and avoidance of centralized systems. Overcollateralized, crypto-backed, non-algorithmic stablecoins are one such medium, similar to the MakerDAO and Dai functionality. Recently, both Aave and Curve have moved forward with plans for similar products.

Aave, the largest money market DeFi application, passed the “Greenlight for GHO” community governance proposal. GHO, Aave’s new stablecoin, will soon have the ability to be minted against a diversified basket of crypto assets. Borrowers of GHO will continue earning interest on the supplied collateral used to mint the new stablecoin. All of the GHO interest payments will be paid back to the DAO treasury and many expect the offering will be a major source of revenue for the DAO.

Curve, one of the largest decentralized exchanges, published the smart contract code for their potential new stablecoin named crvUSD. Curve has the largest total value locked of any decentralized exchange and provides users low fee swaps on stablecoins for minimal slippage. After a code review, a community vote for the stablecoin implementation will likely take place over the next few weeks. Both Aave and Curve would use loans governed by smart contracts, requiring specific loan to value requirements and liquidation ratios, protect the overall health and solvency of the entire system.

Download the Full Weekly Market Review Here