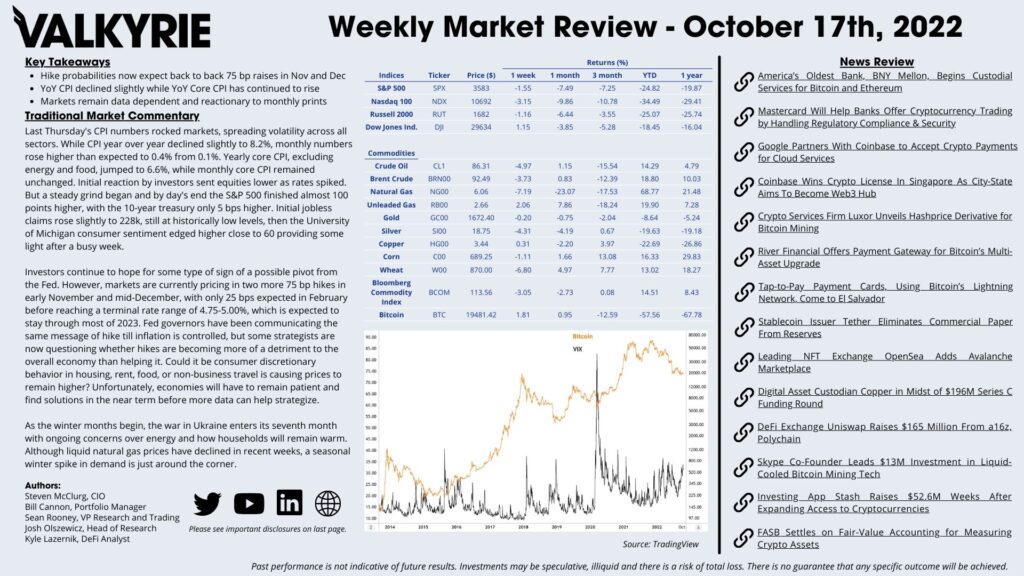

Traditional Market Commentary

- Hike probabilities now expect back to back 75 bp raises in Nov and Dec

- YoY CPI declined slightly while YoY Core CPI has continued to rise

- Markets remain data dependent and reactionary to monthly prints

Last Thursday’s CPI numbers rocked markets, spreading volatility across all sectors. While CPI year over year declined slightly to 8.2%, monthly numbers rose higher than expected to 0.4% from 0.1%. Yearly core CPI, excluding energy and food, jumped to 6.6%, while monthly core CPI remained unchanged. Initial reaction by investors sent equities lower as rates spiked. But a steady grind began and by day’s end the S&P 500 finished almost 100 points higher, with the 10-year treasury only 5 bps higher. Initial jobless claims rose slightly to 228k, still at historically low levels, then the University of Michigan consumer sentiment edged higher close to 60 providing some light after a busy week.

Investors continue to hope for some type of sign of a possible pivot from the Fed. However, markets are currently pricing in two more 75 bp hikes in early November and mid-December, with only 25 bps expected in February before reaching a terminal rate range of 4.75-5.00%, which is expected to stay through most of 2023. Fed governors have been communicating the same message of hike till inflation is controlled, but some strategists are now questioning whether hikes are becoming more of a detriment to the overall economy than helping it. Could it be consumer discretionary behavior in housing, rent, food, or non-business travel is causing prices to remain higher? Unfortunately, economies will have to remain patient and find solutions in the near term before more data can help strategize.

As the winter months begin, the war in Ukraine enters its seventh month with ongoing concerns over energy and how households will remain warm. Although liquid natural gas prices have declined in recent weeks, a seasonal winter spike in demand is just around the corner.

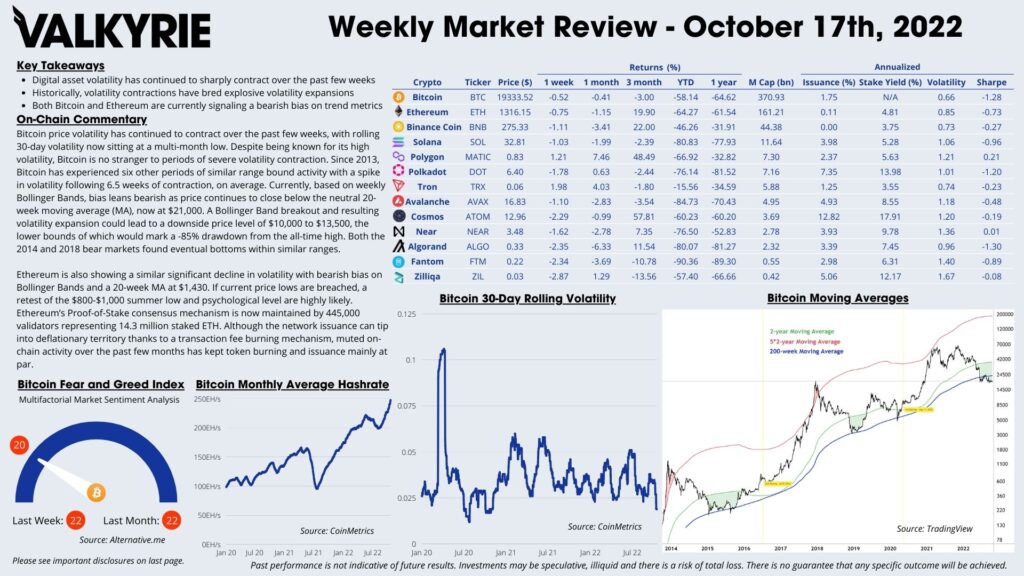

On-Chain Commentary

- Digital asset volatility has continued to sharply contract over the past few weeks

- Historically, volatility contractions have bred explosive volatility expansions

- Both Bitcoin and Ethereum are currently signaling a bearish bias on trend metrics

Bitcoin price volatility has continued to contract over the past few weeks, with rolling 30-day volatility now sitting at a multi-month low. Despite being known for its high volatility, Bitcoin is no stranger to periods of severe volatility contraction. Since 2013, Bitcoin has experienced six other periods of similar range bound activity with a spike in volatility following 6.5 weeks of contraction, on average. Currently, based on weekly Bollinger Bands, bias leans bearish as price continues to close below the neutral 20-week moving average (MA), now at $21,000. A Bollinger Band breakout and resulting volatility expansion could lead to a downside price level of $10,000 to $13,500, the lower bounds of which would mark a -85% drawdown from the all-time high. Both the 2014 and 2018 bear markets found eventual bottoms within similar ranges.

Ethereum is also showing a similar significant decline in volatility with bearish bias on Bollinger Bands and a 20-week MA at $1,430. If current price lows are breached, a retest of the $800-$1,000 summer low and psychological level are highly likely. Ethereum’s Proof-of-Stake consensus mechanism is now maintained by 445,000 validators representing 14.3 million staked ETH. Although the network issuance can tip into deflationary territory thanks to a transaction fee burning mechanism, muted on-chain activity over the past few months has kept token burning and issuance mainly at par.

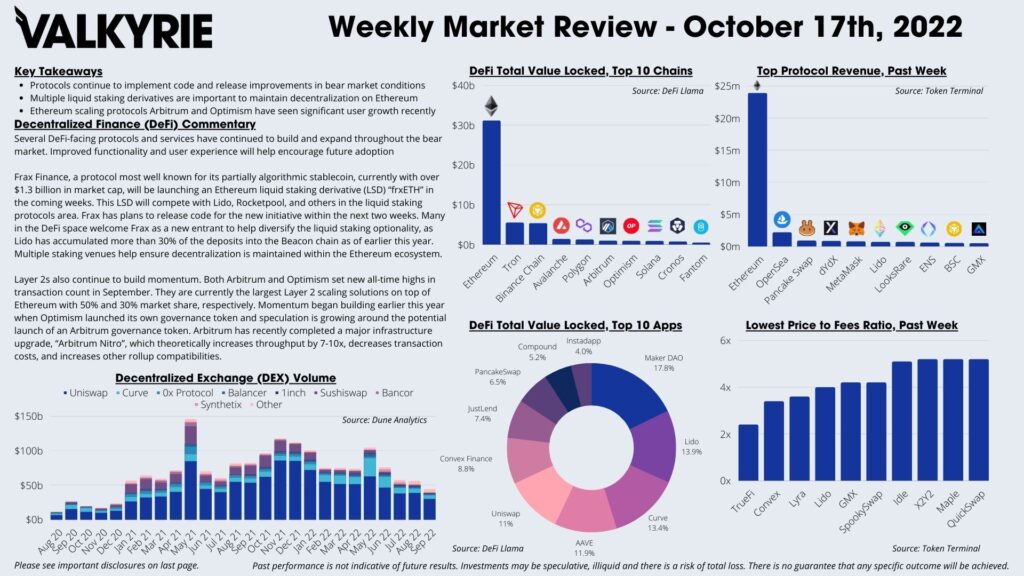

DeFi Commentary

- Protocols continue to implement code and release improvements in bear market conditions

- Multiple liquid staking derivatives are important to maintain decentralization on Ethereum

- Ethereum scaling protocols Arbitrum and Optimism have seen significant user growth recently

Several DeFi-facing protocols and services have continued to build and expand throughout the bear market. Improved functionality and user experience will help encourage future adoption

Frax Finance, a protocol most well known for its partially algorithmic stablecoin, currently with over $1.3 billion in market cap, will be launching an Ethereum liquid staking derivative (LSD) “frxETH” in the coming weeks. This LSD will compete with Lido, Rocketpool, and others in the liquid staking protocols area. Frax has plans to release code for the new initiative within the next two weeks. Many in the DeFi space welcome Frax as a new entrant to help diversify the liquid staking optionality, as Lido has accumulated more than 30% of the deposits into the Beacon chain as of earlier this year. Multiple staking venues help ensure decentralization is maintained within the Ethereum ecosystem.

Layer 2s also continue to build momentum. Both Arbitrum and Optimism set new all-time highs in transaction count in September. They are currently the largest Layer 2 scaling solutions on top of Ethereum with 50% and 30% market share, respectively. Momentum began building earlier this year when Optimism launched its own governance token and speculation is growing around the potential launch of an Arbitrum governance token. Arbitrum has recently completed a major infrastructure upgrade, “Arbitrum Nitro”, which theoretically increases throughput by 7-10x, decreases transaction costs, and increases other rollup compatibilities.

Download the Full Weekly Market Review Here