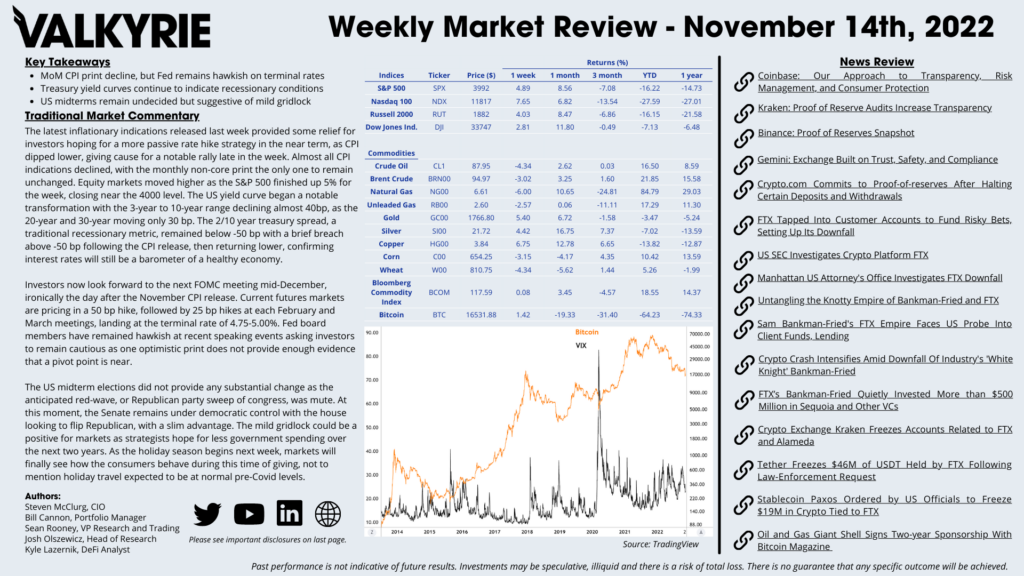

Traditional Market Commentary

- MoM CPI print decline, but Fed remains hawkish on terminal rates

- Treasury yield curves continue to indicate recessionary conditions

- US midterms remain undecided but suggestive of mild gridlock

The latest inflationary indications released last week provided some relief for investors hoping for a more passive rate hike strategy in the near term, as CPI dipped lower, giving cause for a notable rally late in the week. Almost all CPI indications declined, with the monthly non-core print the only one to remain unchanged. Equity markets moved higher as the S&P 500 finished up 5% for the week, closing near the 4000 level. The US yield curve began a notable transformation with the 3-year to 10-year range declining almost 40bp, as the 20-year and 30-year moving only 30 bp. The 2/10 year treasury spread, a traditional recessionary metric, remained below -50 bp with a brief breach above -50 bp following the CPI release, then returning lower, confirming interest rates will still be a barometer of a healthy economy.

Investors now look forward to the next FOMC meeting mid-December, ironically the day after the November CPI release. Current futures markets are pricing in a 50 bp hike, followed by 25 bp hikes at each February and March meetings, landing at the terminal rate of 4.75-5.00%. Fed board members have remained hawkish at recent speaking events asking investors to remain cautious as one optimistic print does not provide enough evidence that a pivot point is near.

The US midterm elections did not provide any substantial change as the anticipated red-wave, or Republican party sweep of congress, was mute. At this moment, the Senate remains under democratic control with the house looking to flip Republican, with a slim advantage. The mild gridlock could be a positive for markets as strategists hope for less government spending over the next two years. As the holiday season begins next week, markets will finally see how the consumers behave during this time of giving, not to mention holiday travel expected to be at normal pre-Covid levels.

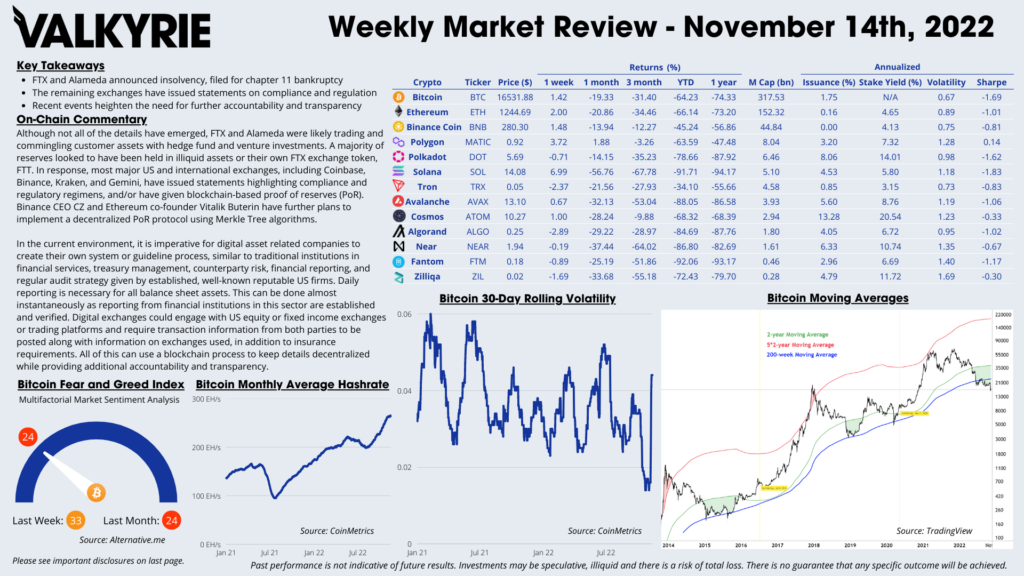

On-Chain Commentary

- FTX and Alameda announced insolvency, filed for chapter 11 bankruptcy

- The remaining exchanges have issued statements on compliance and regulation

- Recent events heighten the need for further accountability and transparency

Although not all of the details have emerged, FTX and Alameda were likely trading and commingling customer assets with hedge fund and venture investments. A majority of reserves looked to have been held in illiquid assets or their own FTX exchange token, FTT. In response, most major US and international exchanges, including Coinbase, Binance, Kraken, and Gemini, have issued statements highlighting compliance and regulatory regimens, and/or have given blockchain-based proof of reserves (PoR). Binance CEO CZ and Ethereum co-founder Vitalik Buterin have further plans to implement a decentralized PoR protocol using Merkle Tree algorithms.

In the current environment, it is imperative for digital asset related companies to create their own system or guideline process, similar to traditional institutions in financial services, treasury management, counterparty risk, financial reporting, and regular audit strategy given by established, well-known reputable US firms. Daily reporting is necessary for all balance sheet assets. This can be done almost instantaneously as reporting from financial institutions in this sector are established and verified. Digital exchanges could engage with US equity or fixed income exchanges or trading platforms and require transaction information from both parties to be posted along with information on exchanges used, in addition to insurance requirements. All of this can use a blockchain process to keep details decentralized while providing additional accountability and transparency.