Traditional Market Commentary

- The Fed and Jerome Powell remain firmly hawkish in the near term

- Terminal Fed Funds Rate is likely to exceed 5.00% over the next year

- US midterm elections and CPI will likely bring further volatility this week

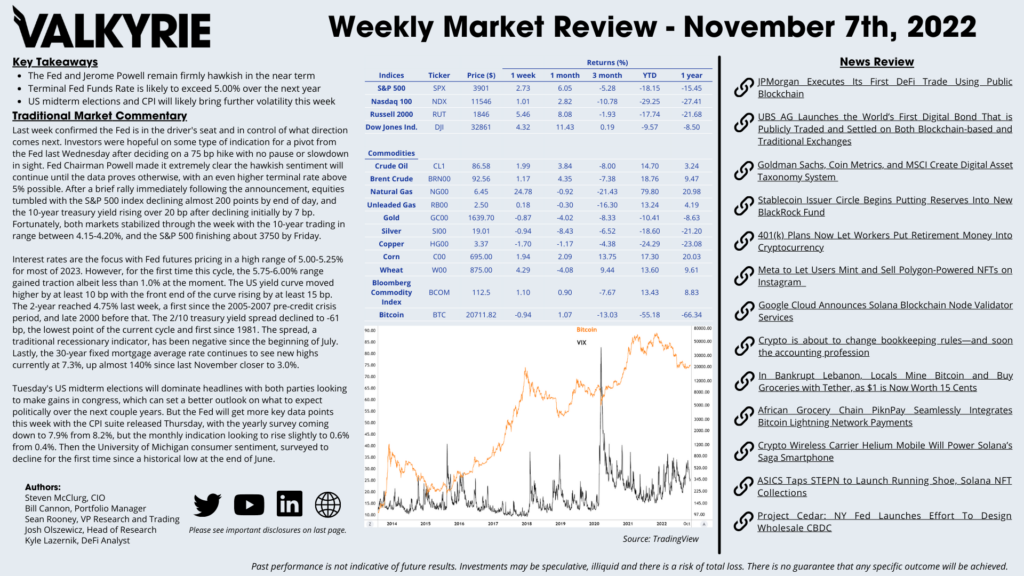

Last week confirmed the Fed is in the driver’s seat and in control of what direction comes next. Investors were hopeful on some type of indication for a pivot from the Fed last Wednesday after deciding on a 75 bp hike with no pause or slowdown in sight. Fed Chairman Powell made it extremely clear the hawkish sentiment will continue until the data proves otherwise, with an even higher terminal rate above 5% possible. After a brief rally immediately following the announcement, equities tumbled with the S&P 500 index declining almost 200 points by end of day, and the 10-year treasury yield rising over 20 bp after declining initially by 7 bp. Fortunately, both markets stabilized through the week with the 10-year trading in range between 4.15-4.20%, and the S&P 500 finishing about 3750 by Friday.

Interest rates are the focus with Fed futures pricing in a high range of 5.00-5.25% for most of 2023. However, for the first time this cycle, the 5.75-6.00% range gained traction albeit less than 1.0% at the moment. The US yield curve moved higher by at least 10 bp with the front end of the curve rising by at least 15 bp. The 2-year reached 4.75% last week, a first since the 2005-2007 pre-credit crisis period, and late 2000 before that. The 2/10 treasury yield spread declined to -61 bp, the lowest point of the current cycle and first since 1981. The spread, a traditional recessionary indicator, has been negative since the beginning of July. Lastly, the 30-year fixed mortgage average rate continues to see new highs currently at 7.3%, up almost 140% since last November closer to 3.0%.

Tuesday’s US midterm elections will dominate headlines with both parties looking to make gains in congress, which can set a better outlook on what to expect politically over the next couple years. But the Fed will get more key data points this week with the CPI suite released Thursday, with the yearly survey coming down to 7.9% from 8.2%, but the monthly indication looking to rise slightly to 0.6% from 0.4%. Then the University of Michigan consumer sentiment, surveyed to decline for the first time since a historical low at the end of June.

On-Chain Commentary

- Traditional finance continues to become more comfortable with digital assets

- Polygon (MATIC) has remained a strong overperformer after business integrations

- Bitcoin’s multi-month volatility squeeze remains unchanged, set for a move by EoY

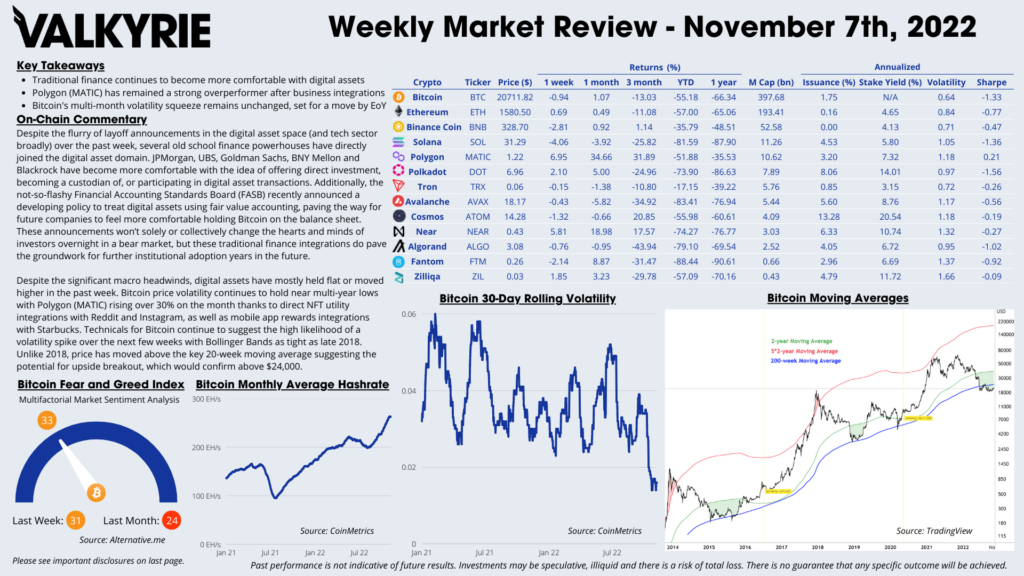

Despite the flurry of layoff announcements in the digital asset space (and tech sector broadly) over the past week, several old school finance powerhouses have directly joined the digital asset domain. JPMorgan, UBS, Goldman Sachs, BNY Mellon and Blackrock have become more comfortable with the idea of offering direct investment, becoming a custodian of, or participating in digital asset transactions. Additionally, the not-so-flashy Financial Accounting Standards Board (FASB) recently announced a developing policy to treat digital assets using fair value accounting, paving the way for future companies to feel more comfortable holding Bitcoin on the balance sheet. These announcements won’t solely or collectively change the hearts and minds of investors overnight in a bear market, but these traditional finance integrations do pave the groundwork for further institutional adoption years in the future.

Despite the significant macro headwinds, digital assets have mostly held flat or moved higher in the past week. Bitcoin price volatility continues to hold near multi-year lows with Polygon (MATIC) rising over 30% on the month thanks to direct NFT utility integrations with Reddit and Instagram, as well as mobile app rewards integrations with Starbucks. Technicals for Bitcoin continue to suggest the high likelihood of a volatility spike over the next few weeks with Bollinger Bands as tight as late 2018. Unlike 2018, price has moved above the key 20-week moving average suggesting the potential for upside breakout, which would confirm above $24,000.