Traditional Market Commentary

Key Takeaways

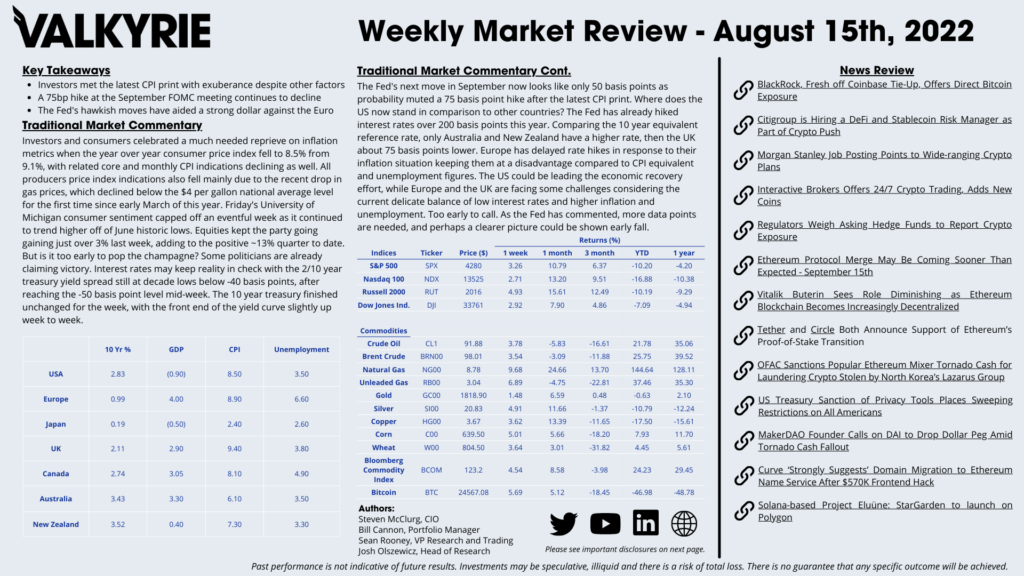

- Investors met the latest CPI print with exuberance despite other factors

- A 75bp hike at the September FOMC meeting continues to decline

- The Fed’s hawkish moves have aided a strong dollar against the Euro

Investors and consumers celebrated a much needed reprieve on inflation metrics when the year over year consumer price index fell to 8.5% from 9.1%, with related core and monthly CPI indications declining as well. All producers price index indications also fell mainly due to the recent drop in gas prices, which declined below the $4 per gallon national average level for the first time since early March of this year. Friday’s University of Michigan consumer sentiment capped off an eventful week as it continued to trend higher off of June historic lows. Equities kept the party going gaining just over 3% last week, adding to the positive ~13% quarter to date. But is it too early to pop the champagne? Some politicians are already claiming victory. Interest rates may keep reality in check with the 2/10 year treasury yield spread still at decade lows below -40 basis points, after reaching the -50 basis point level mid-week. The 10 year treasury finished unchanged for the week, with the front end of the yield curve slightly up week to week.

The Fed’s next move in September now looks like only 50 basis points as probability muted a 75 basis point hike after the latest CPI print. Where does the US now stand in comparison to other countries? The Fed has already hiked interest rates over 200 basis points this year. Comparing the 10 year equivalent reference rate, only Australia and New Zealand have a higher rate, then the UK about 75 basis points lower. Europe has delayed rate hikes in response to their inflation situation keeping them at a disadvantage compared to CPI equivalent and unemployment figures. The US could be leading the economic recovery effort, while Europe and the UK are facing some challenges considering the current delicate balance of low interest rates and higher inflation and unemployment. Too early to call. As the Fed has commented, more data points are needed, and perhaps a clearer picture could be shown early fall.

On-Chain Commentary

Key Takeaways

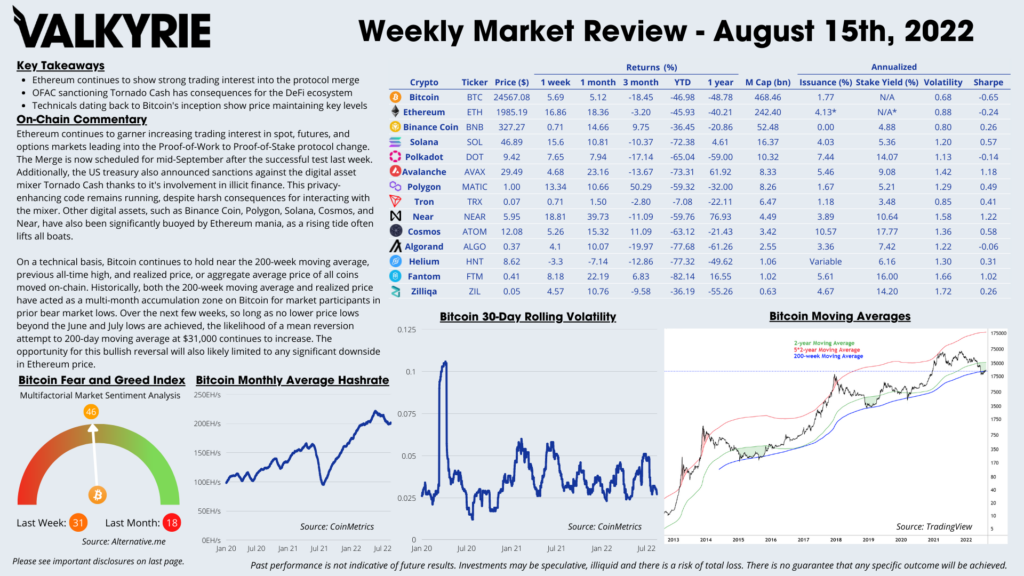

- Ethereum continues to show strong trading interest into the protocol merge

- OFAC sanctioning Tornado Cash has consequences for the DeFi ecosystem

- Technicals dating back to Bitcoin’s inception show price maintaining key levels

Ethereum continues to garner increasing trading interest in spot, futures, and options markets leading into the Proof-of-Work to Proof-of-Stake protocol change. The Merge is now scheduled for mid-September after the successful test last week. Additionally, the US treasury also announced sanctions against the digital asset mixer Tornado Cash thanks to it’s involvement in illicit finance. This privacy-enhancing code remains running, despite harsh consequences for interacting with the mixer. Other digital assets, such as Binance Coin, Polygon, Solana, Cosmos, and Near, have also been significantly buoyed by Ethereum mania.

On a technical basis, Bitcoin continues to hold near the 200-week moving average, previous all-time high, and realized price, or aggregate average price of all coins moved on-chain. Historically, both the 200-week moving average and realized price have acted as a multi-month accumulation zone on Bitcoin for market participants in prior bear market lows. Over the next few weeks, so long as no lower price lows beyond the June and July lows are achieved, the likelihood of a mean reversion attempt to 200-day moving average at $31,000 continues to increase. The opportunity for this bullish reversal will also likely be limited to any significant downside in Ethereum price.

Download the Full Weekly Market Review Here