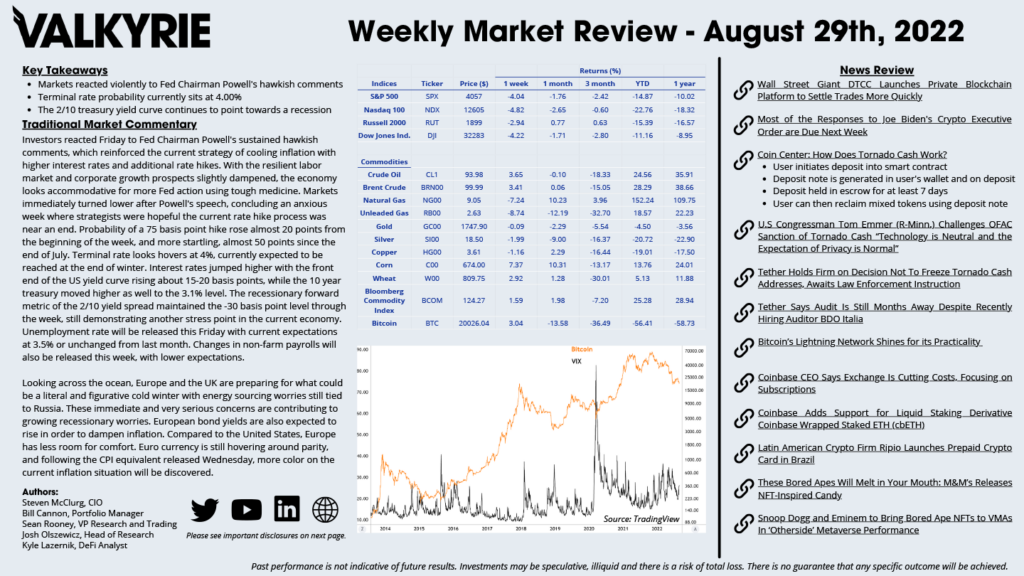

Traditional Market Commentary

- Markets reacted violently to Fed Chairman Powell’s hawkish comments

- Terminal rate probability currently sits at 4.00%

- The 2/10 treasury yield curve continues to point towards a recession

Investors reacted Friday to Fed Chairman Powell’s sustained hawkish comments, which reinforced the current strategy of cooling inflation with higher interest rates and additional rate hikes. With the resilient labor market and corporate growth prospects slightly dampened, the economy looks accommodative for more Fed action using tough medicine. Markets immediately turned lower after Powell’s speech, concluding an anxious week where strategists were hopeful the current rate hike process was near an end. Probability of a 75 basis point hike rose almost 20 points from the beginning of the week, and more startling, almost 50 points since the end of July. Terminal rate looks hovers at 4%, currently expected to be reached at the end of winter. Interest rates jumped higher with the front end of the US yield curve rising about 15-20 basis points, while the 10 year treasury moved higher as well to the 3.1% level. The recessionary forward metric of the 2/10 yield spread maintained the -30 basis point level through the week, still demonstrating another stress point in the current economy. Unemployment rate will be released this Friday with current expectations at 3.5% or unchanged from last month. Changes in non-farm payrolls will also be released this week, with lower expectations.

Looking across the ocean, Europe and the UK are preparing for what could be a literal and figurative cold winter with energy sourcing worries still tied to Russia. These immediate and very serious concerns are contributing to growing recessionary worries. European bond yields are also expected to rise in order to dampen inflation. Compared to the United States, Europe has less room for comfort. Euro currency is still hovering around parity, and following the CPI equivalent released Wednesday, more color on the current inflation situation will be discovered.

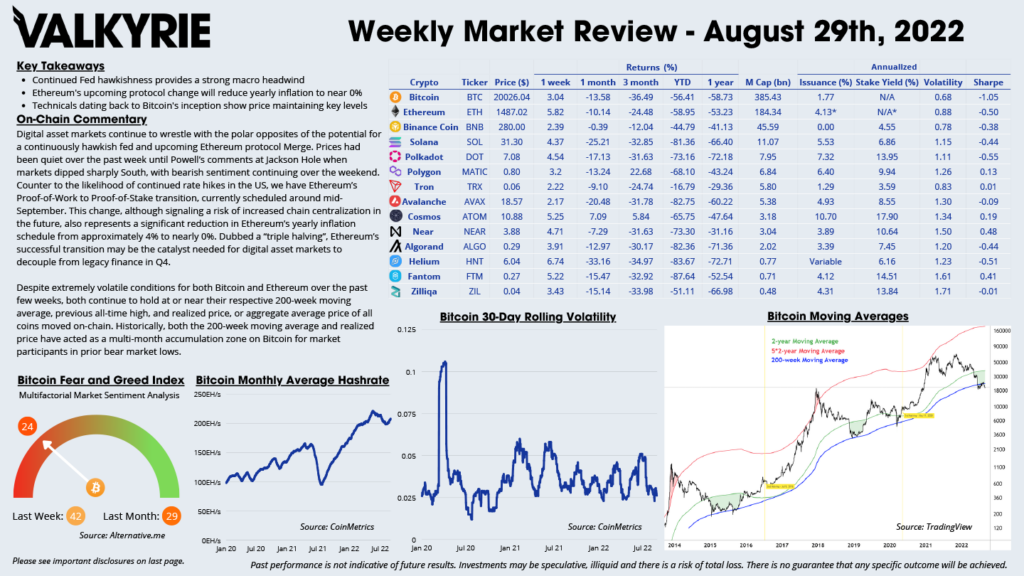

On-Chain Commentary

- Continued Fed hawkishness provides a strong macro headwind

- Ethereum’s upcoming protocol change will reduce yearly inflation to near 0%

- Technicals dating back to Bitcoin’s inception show price maintaining key levels

Digital asset markets continue to wrestle with the polar opposites of the potential for a continuously hawkish fed and upcoming Ethereum protocol Merge. Prices had been quiet over the past week until Powell’s comments at Jackson Hole when markets dipped sharply South, with bearish sentiment continuing over the weekend. Counter to the likelihood of continued rate hikes in the US, we have Ethereum’s Proof-of-Work to Proof-of-Stake transition, currently scheduled around mid-September. This change, although signaling a risk of increased chain centralization in the future, also represents a significant reduction in Ethereum’s yearly inflation schedule from approximately 4% to nearly 0%. Dubbed a “triple halving”, Ethereum’s successful transition may be the catalyst needed for digital asset markets to decouple from legacy finance in Q4.

Despite extremely volatile conditions for both Bitcoin and Ethereum over the past few weeks, both continue to hold at or near their respective 200-week moving average, previous all-time high, and realized price, or aggregate average price of all coins moved on-chain. Historically, both the 200-week moving average and realized price have acted as a multi-month accumulation zone on Bitcoin for market participants in prior bear market lows.

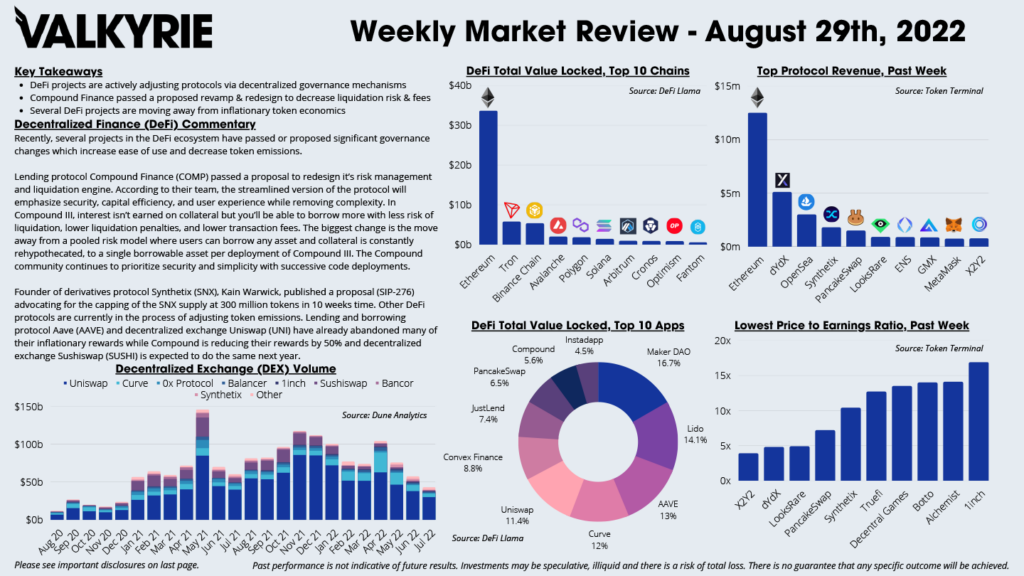

DeFi Commentary

- DeFi projects are actively adjusting protocols via decentralized governance mechanisms

- Compound Finance passed a proposed revamp & redesign to decrease liquidation risk & fees

- Several DeFi projects are moving away from inflationary token economics

Recently, several projects in the DeFi ecosystem have passed or proposed significant governance changes which increase ease of use and decrease token emissions.

Lending protocol Compound Finance (COMP) passed a proposal to redesign it’s risk management and liquidation engine. According to their team, the streamlined version of the protocol will emphasize security, capital efficiency, and user experience while removing complexity. In Compound III, interest isn’t earned on collateral but you’ll be able to borrow more with less risk of liquidation, lower liquidation penalties, and lower transaction fees. The biggest change is the move away from a pooled risk model where users can borrow any asset and collateral is constantly rehypothecated, to a single borrowable asset per deployment of Compound III. The Compound community continues to prioritize security and simplicity with successive code deployments.

Founder of derivatives protocol Synthetix (SNX), Kain Warwick, published a proposal (SIP-276) advocating for the capping of the SNX supply at 300 million tokens in 10 weeks time. Other DeFi protocols are currently in the process of adjusting token emissions. Lending and borrowing protocol Aave (AAVE) and decentralized exchange Uniswap (UNI) have already abandoned many of their inflationary rewards while Compound is reducing their rewards by 50% and decentralized exchange Sushiswap (SUSHI) is expected to do the same next year.

Download the Full Weekly Market Review Here