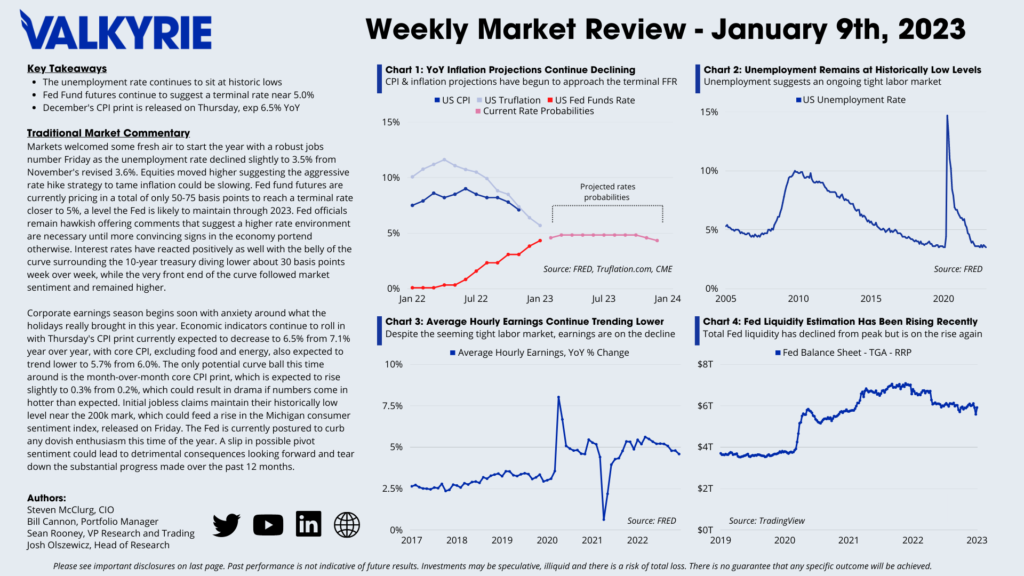

Traditional Market Commentary

- The unemployment rate continues to sit at historic lows

- Fed Fund futures continue to suggest a terminal rate near 5.0%

- December’s CPI print is released on Thursday, exp 6.5% YoY

Markets welcomed some fresh air to start the year with a robust jobs number Friday as the unemployment rate declined slightly to 3.5% from November’s revised 3.6%. Equities moved higher suggesting the aggressive rate hike strategy to tame inflation could be slowing. Fed fund futures are currently pricing in a total of only 50-75 basis points to reach a terminal rate closer to 5%, a level the Fed is likely to maintain through 2023. Fed officials remain hawkish offering comments that suggest a higher rate environment are necessary until more convincing signs in the economy portend otherwise. Interest rates have reacted positively as well with the belly of the curve surrounding the 10-year treasury diving lower about 30 basis points week over week, while the very front end of the curve followed market sentiment and remained higher.

Corporate earnings season begins soon with anxiety around what the holidays really brought in this year. Economic indicators continue to roll in with Thursday’s CPI print currently expected to decrease to 6.5% from 7.1% year over year, with core CPI, excluding food and energy, also expected to trend lower to 5.7% from 6.0%. The only potential curve ball this time around is the month-over-month core CPI print, which is expected to rise slightly to 0.3% from 0.2%, which could result in drama if numbers come in hotter than expected. Initial jobless claims maintain their historically low level near the 200k mark, which could feed a rise in the Michigan consumer sentiment index, released on Friday. The Fed is currently postured to curb any dovish enthusiasm this time of the year. A slip in possible pivot sentiment could lead to detrimental consequences looking forward and tear down the substantial progress made over the past 12 months.

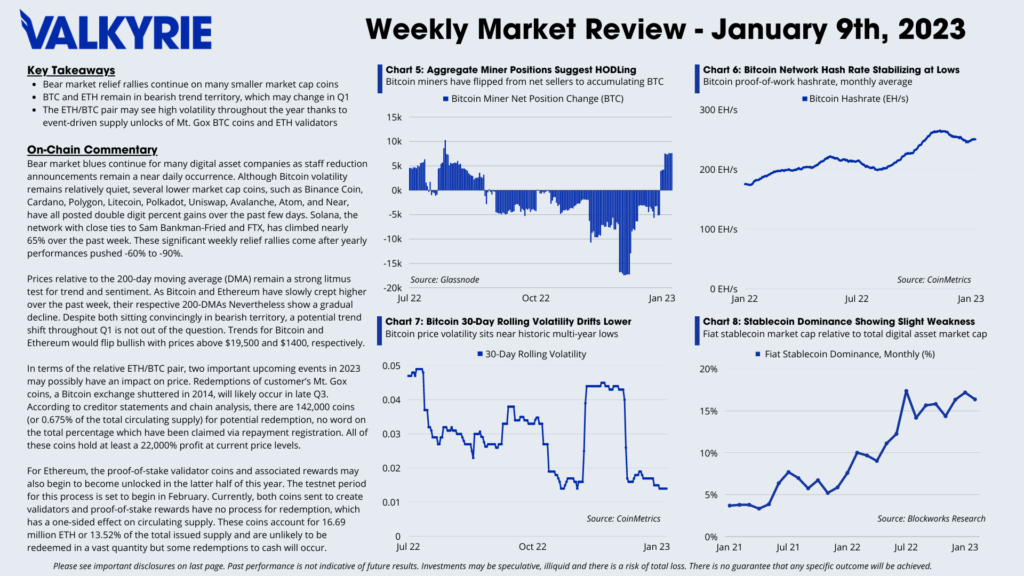

On-Chain Commentary

- Bear market relief rallies continue on many smaller market cap coins

- BTC and ETH remain in bearish trend territory, which may change in Q1

- The ETH/BTC pair may see high volatility throughout the year thanks to event-driven supply unlocks of Mt. Gox BTC coins and ETH validators

Bear market blues continue for many digital asset companies as staff reduction announcements remain a near daily occurrence. Although Bitcoin volatility remains relatively quiet, several lower market cap coins, such as Binance Coin, Cardano, Polygon, Litecoin, Polkadot, Uniswap, Avalanche, Atom, and Near, have all posted double digit percent gains over the past few days. Solana, the network with close ties to Sam Bankman-Fried and FTX, has climbed nearly 65% over the past week. These significant weekly relief rallies come after yearly performances pushed -60% to -90%.

Prices relative to the 200-day moving average (DMA) remain a strong litmus test for trend and sentiment. As Bitcoin and Ethereum have slowly crept higher over the past week, their respective 200-DMAs Nevertheless show a gradual decline. Despite both sitting convincingly in bearish territory, a potential trend shift throughout Q1 is not out of the question. Trends for Bitcoin and Ethereum would flip bullish with prices above $19,500 and $1400, respectively.

In terms of the relative ETH/BTC pair, two important upcoming events in 2023 may possibly have an impact on price. Redemptions of customer’s Mt. Gox coins, a Bitcoin exchange shuttered in 2014, will likely occur in late Q3. According to creditor statements and chain analysis, there are 142,000 coins (or 0.675% of the total circulating supply) for potential redemption, no word on the total percentage which have been claimed via repayment registration. All of these coins hold at least a 22,000% profit at current price levels.

For Ethereum, the proof-of-stake validator coins and associated rewards may also begin to become unlocked in the latter half of this year. The testnet period for this process is set to begin in February. Currently, both coins sent to create validators and proof-of-stake rewards have no process for redemption, which has a one-sided effect on circulating supply. These coins account for 16.69 million ETH or 13.52% of the total issued supply and are unlikely to be redeemed in a vast quantity but some redemptions to cash will occur.