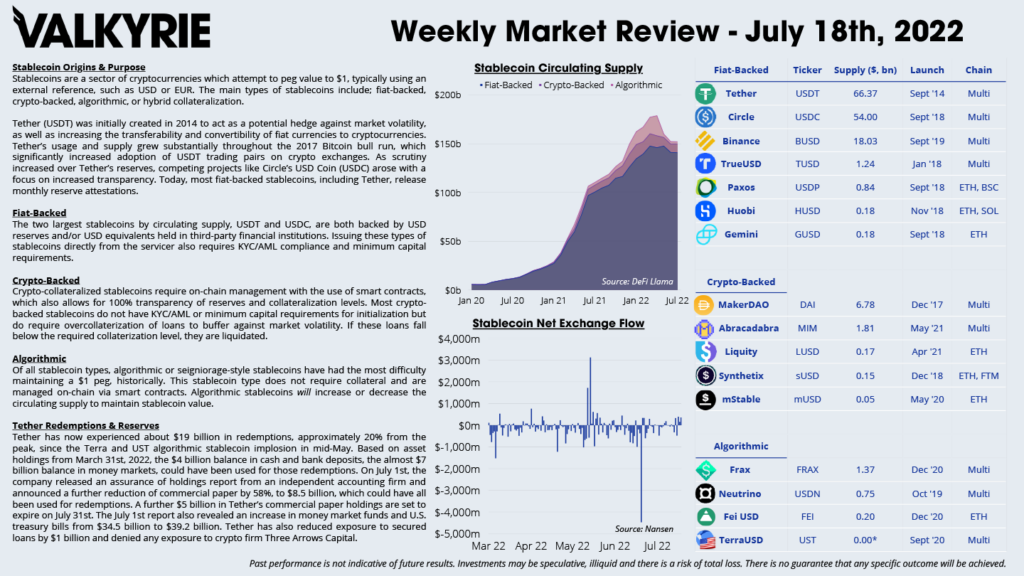

Macro Commentary

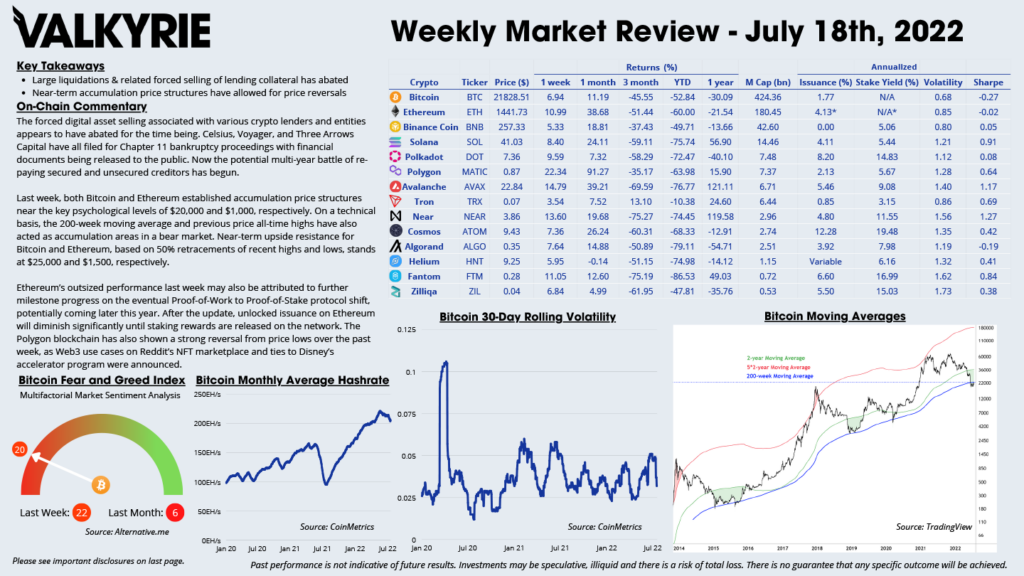

Key Takeaways

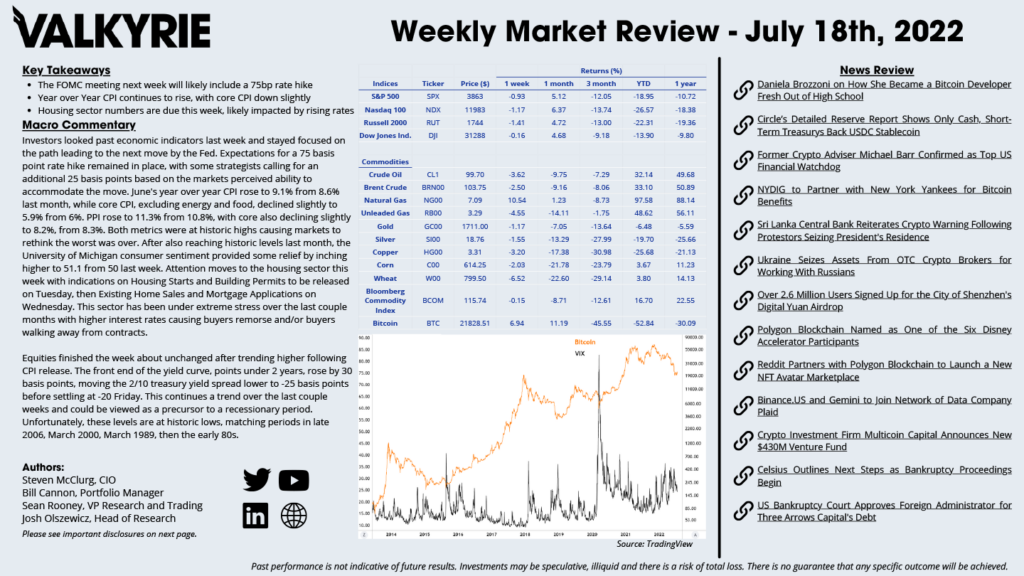

- The FOMC meeting next week will likely include a 75bp rate hike

- Year over Year CPI continues to rise, with core CPI down slightly

- Housing sector numbers are due this week, likely impacted by rising rates

Investors looked past economic indicators last week and stayed focused on the path leading to the next move by the Fed. Expectations for a 75 basis point rate hike remained in place, with some strategists calling for an additional 25 basis points based on the markets perceived ability to accommodate the move. June’s year over year CPI rose to 9.1% from 8.6% last month, while core CPI, excluding energy and food, declined slightly to 5.9% from 6%. PPI rose to 11.3% from 10.8%, with core also declining slightly to 8.2%, from 8.3%. Both metrics were at historic highs causing markets to rethink the worst was over. After also reaching historic levels last month, the University of Michigan consumer sentiment provided some relief by inching higher to 51.1 from 50 last week. Attention moves to the housing sector this week with indications on Housing Starts and Building Permits to be released on Tuesday, then Existing Home Sales and Mortgage Applications on Wednesday. This sector has been under extreme stress over the last couple months with higher interest rates causing buyers remorse and/or buyers walking away from contracts.

Equities finished the week about unchanged after trending higher following CPI release. The front end of the yield curve, points under 2 years, rose by 30 basis points, moving the 2/10 treasury yield spread lower to -25 basis points before settling at -20 Friday. This continues a trend over the last couple weeks and could be viewed as a precursor to a recessionary period. Unfortunately, these levels are at historic lows, matching periods in late 2006, March 2000, March 1989, then the early 80s.

On-Chain Commentary

Key Takeaways

- Large liquidations & related forced selling of lending collateral has abated

- Near-term accumulation price structures have allowed for price reversals

The forced digital asset selling associated with various crypto lenders and entities appears to have abated for the time being. Celsius, Voyager, and Three Arrows Capital have all filed for Chapter 11 bankruptcy proceedings with financial documents being released to the public. Now the potential multi-year battle of re-paying secured and unsecured creditors has begun.

Last week, both Bitcoin and Ethereum established accumulation price structures near the key psychological levels of $20,000 and $1,000, respectively. On a technical basis, the 200-week moving average and previous price all-time highs have also acted as accumulation areas in a bear market. Near-term upside resistance for Bitcoin and Ethereum, based on 50% retracements of recent highs and lows, stands at $25,000 and $1,500, respectively.

Ethereum’s outsized performance last week may also be attributed to further milestone progress on the eventual Proof-of-Work to Proof-of-Stake protocol shift, potentially coming later this year. After the update, unlocked issuance on Ethereum will diminish significantly until staking rewards are released on the network. The Polygon blockchain has also shown a strong reversal from price lows over the past week, as Web3 use cases on Reddit’s NFT marketplace and ties to Disney’s accelerator program were announced.

Download the Full Weekly Market Review Here

The Portfolio Management Team

Steven McClurg, CIO

Bill Cannon, Portfolio Manager

Wes Cowan, Portfolio Manager, Head of Defi

Josh Olszewicz, Head of Research

Sean Rooney, VP Research and Trading

Will McDonough, Vice Chairman, Investment Committee

Leah Wald, CEO, Investment Committee

Shannon Smith, Head of Investor Relations