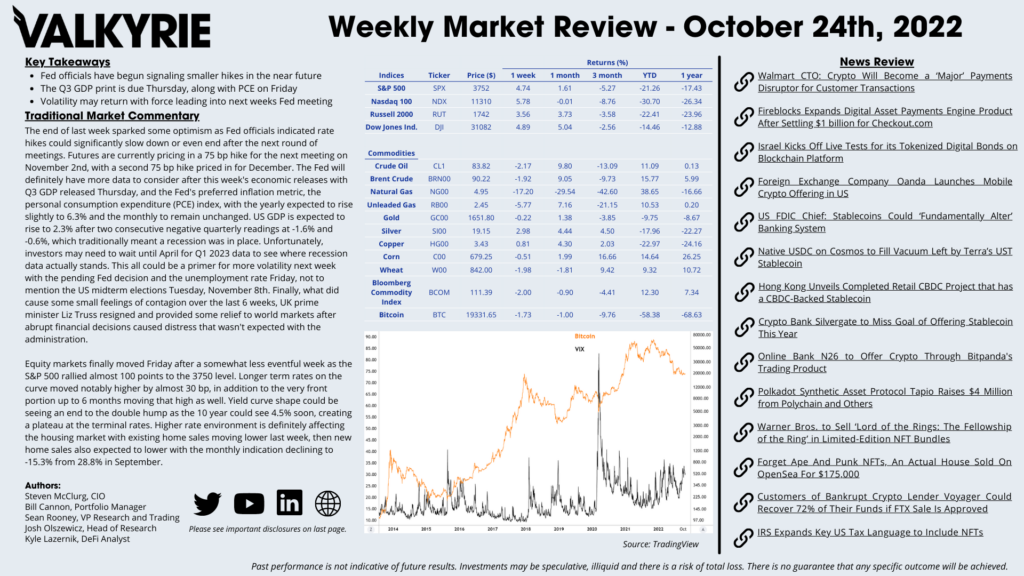

Traditional Market Commentary

- Fed officials have begun signaling smaller hikes in the near future

- The Q3 GDP print is due Thursday, along with PCE on Friday

- Volatility may return with force leading into next weeks Fed meeting

The end of last week sparked some optimism as Fed officials indicated rate hikes could significantly slow down or even end after the next round of meetings. Futures are currently pricing in a 75 bp hike for the next meeting on November 2nd, with a second 75 bp hike priced in for December. The Fed will definitely have more data to consider after this week’s economic releases with Q3 GDP released Thursday, and the Fed’s preferred inflation metric, the personal consumption expenditure (PCE) index, with the yearly expected to rise slightly to 6.3% and the monthly to remain unchanged. US GDP is expected to rise to 2.3% after two consecutive negative quarterly readings at -1.6% and -0.6%, which traditionally meant a recession was in place. Unfortunately, investors may need to wait until April for Q1 2023 data to see where recession data actually stands. This all could be a primer for more volatility next week with the pending Fed decision and the unemployment rate Friday, not to mention the US midterm elections Tuesday, November 8th. Finally, what did cause some small feelings of contagion over the last 6 weeks, UK prime minister Liz Truss resigned and provided some relief to world markets after abrupt financial decisions caused distress that wasn’t expected with the administration.

Equity markets finally moved Friday after a somewhat less eventful week as the S&P 500 rallied almost 100 points to the 3750 level. Longer term rates on the curve moved notably higher by almost 30 bp, in addition to the very front portion up to 6 months moving that high as well. Yield curve shape could be seeing an end to the double hump as the 10 year could see 4.5% soon, creating a plateau at the terminal rates. Higher rate environment is definitely affecting the housing market with existing home sales moving lower last week, then new home sales also expected to lower with the monthly indication declining to -15.3% from 28.8% in September.

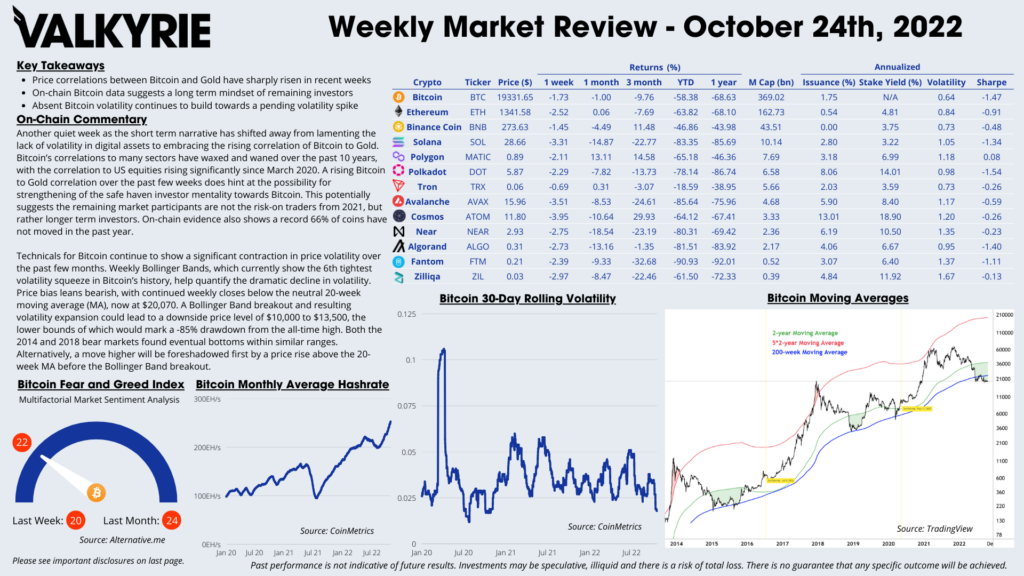

On-Chain Commentary

- Price correlations between Bitcoin and Gold have sharply risen in recent weeks

- On-chain Bitcoin data suggests a long term mindset of remaining investors

- Absent Bitcoin volatility continues to build towards a pending volatility spike

Another quiet week as the short term narrative has shifted away from lamenting the lack of volatility in digital assets to embracing the rising correlation of Bitcoin to Gold. Bitcoin’s correlations to many sectors have waxed and waned over the past 10 years, with the correlation to US equities rising significantly since March 2020. A rising Bitcoin to Gold correlation over the past few weeks does hint at the possibility for strengthening of the safe haven investor mentality towards Bitcoin. This potentially suggests the remaining market participants are not the risk-on traders from 2021, but rather longer term investors. On-chain evidence also shows a record 66% of coins have not moved in the past year.

Technicals for Bitcoin continue to show a significant contraction in price volatility over the past few months. Weekly Bollinger Bands, which currently show the 6th tightest volatility squeeze in Bitcoin’s history, help quantify the dramatic decline in volatility. Price bias leans bearish, with continued weekly closes below the neutral 20-week moving average (MA), now at $20,070. A Bollinger Band breakout and resulting volatility expansion could lead to a downside price level of $10,000 to $13,500, the lower bounds of which would mark a -85% drawdown from the all-time high. Both the 2014 and 2018 bear markets found eventual bottoms within similar ranges. Alternatively, a move higher will be foreshadowed first by a price rise above the 20-week MA before the Bollinger Band breakout.

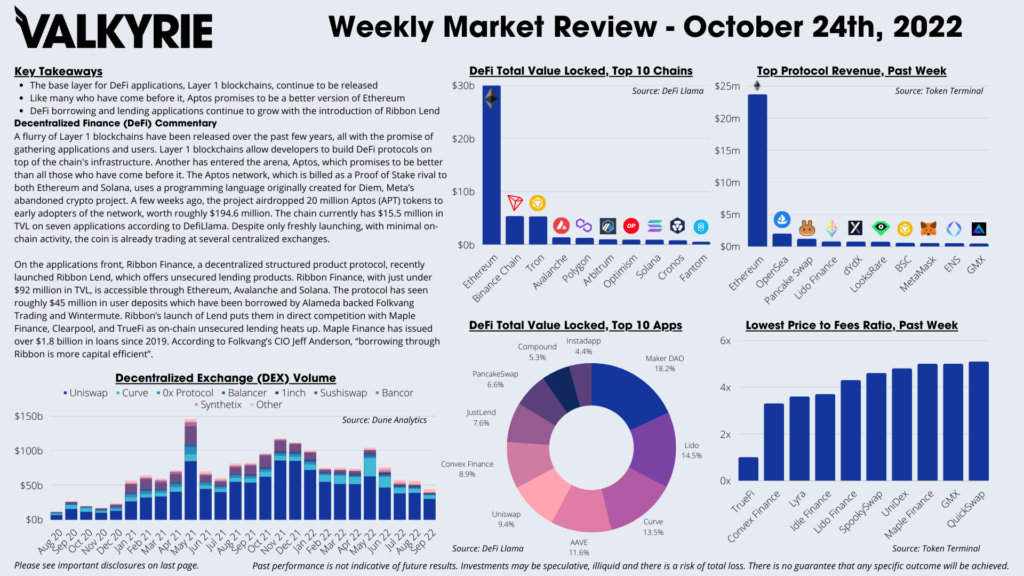

DeFi Commentary

- The base layer for DeFi applications, Layer 1 blockchains, continue to be released

- Like many who have come before it, Aptos promises to be a better version of Ethereum

- DeFi borrowing and lending applications continue to grow with the introduction of Ribbon Lend

A flurry of Layer 1 blockchains have been released over the past few years, all with the promise of gathering applications and users. Layer 1 blockchains allow developers to build DeFi protocols on top of the chain’s infrastructure. Another has entered the arena, Aptos, which promises to be better than all those who have come before it. The Aptos network, which is billed as a Proof of Stake rival to both Ethereum and Solana, uses a programming language originally created for Diem, Meta’s abandoned crypto project. A few weeks ago, the project airdropped 20 million Aptos (APT) tokens to early adopters of the network, worth roughly $194.6 million. The chain currently has $15.5 million in TVL on seven applications according to DefiLlama. Despite only freshly launching, with minimal on-chain activity, the coin is already trading at several centralized exchanges.

On the applications front, Ribbon Finance, a decentralized structured product protocol, recently launched Ribbon Lend, which offers unsecured lending products. Ribbon Finance, with just under $92 million in TVL, is accessible through Ethereum, Avalanche and Solana. The protocol has seen roughly $45 million in user deposits which have been borrowed by Alameda backed Folkvang Trading and Wintermute. Ribbon’s launch of Lend puts them in direct competition with Maple Finance, Clearpool, and TrueFi as on-chain unsecured lending heats up. Maple Finance has issued over $1.8 billion in loans since 2019. According to Folkvang’s CIO Jeff Anderson, “borrowing through Ribbon is more capital efficient”.

Download the Full Weekly Market Review Here